The Morning Hark - 9 Nov 2023

Today’s focus...Powell takes a pass but what about today? Central bankers stick to the script. China back into deflationary territory.

Please note that the Harkster Research Platform had some technical upgrades over the weekend. You may need to hard refresh your browser tab or re-download your Harkster iOS app for the platform to work correctly. See here for more details.

Overnight Highlights

Prices are at 7.00 GMT/2.00 EST, with changes reflecting movement from midnight GMT

Oil - Brent and Crude January futures steadying a touch in Asia but the trend is very much to the downside. The pair currently sitting up a touch at 80 and 75.60 respectively. The Middle East war premium is all but a distant memory as the demand side continues to weigh on the sector. On top of the poor Chinese trade numbers, the stronger USD and the big build in crude stockpiles via the latest API data, today we received the news of China entering deflationary territory. The misery for oil continues.

EQ - Asian equity markets mixed overnight with the deflationary China inflation print weighing on the Hang Seng down around half a percent at 17,570. The Nikkei fairing better and getting some wings from the US indicies strong performances of late. Currently up one percent at 32,650.

The US indicies flat in Asia but still very much holding onto their recent gains with the Nasdaq and S&P futures at 15,390 and 4400 respectively. The S&P currently on its best winning streak in 2 years. Jay you going to break it?

Gold - Gold Dec also flat in Asia currently at 1955 as the safe haven trade continues to leak.

FI - Global yields softer in Asia ahead of Powell (if he fancies it). The US2y and US10y currently trading at 4.93% and 4.51% respectively. As we spoke of in the Week Ahead those tighter financial conditions have been eroded in double quick time. Does that then mean the Fed is back doing the “heavy lifting”? Powell to opine?

European yields following the US lower again although not as pronounced as the US move with the more hawkish tone of the ECB speakers tempering it somewhat. German 10y yields closing lower at 2.62% and the Italian 10y yield similarly at 4.47%.

UK gilt yields likewise with it closing at 4.24%.

FX - USD in somewhat of a holding pattern with the USD Index currently flat at 105.52. The JPY, EUR and GBP all flat versus the USD currently at 150.80, 1.0710 and 1.2290 respectively.

FX option expiries of note for today. USDJPY sees $1.1bn rolling off at 151 and $3bn at 150 if we venture lower again. EUR wise €2bn at 1.07.

Others - Bitcoin and Ethereum up overnight. Bitcoin rising over four percent at 36,760 with news that the SEC is entering the first window to approve all 12 spot Bitcoin ETFs. Ethereum happy to come along for the ride up close to three percent at 1925.

Macro Themes At Play

Recap

Once again not a lot to get our teeth into re economic data.

Central banker wise the ECB shower all tried to temper the market’s enthusiasm regarding rate cuts with all the usual higher for longer, too early to chat about rate cuts. Funnily enough none of them gave a nod to the IMF’s earlier comments from yesterday!

BoE’s Bailey was a repeat of the odious toad’s comments last week post BoE. So pinch of salt required I would hazard.

Fed wise however big fat doughnut from Powell so I guess we roll expectations into his speech today. His underlings added little further to the debate other than caution, higher for longer and may need to do more.

One other thing of note from yesterday. The 30y US mortgage rate, which had us all in a bit of a kerfuffle a few weeks back as it approached then conquered 8%, is now clocking in at 7.61%. The largest weekly drop in 16 months.

Eurozone Retail Sales for September were pretty much in line and a bit of a history lesson.

The National Bank of Poland, somewhat surprisingly, decided to skip a further cut for now and held rates steady at 5.75%.

The Bank of Canada Summary of Deliberations had some points of note:

Near term inflation expectations have been easing but longer term expectations remain well anchored;

Persistent core inflation, elevated inflation expectations and wage growth could initiate higher inflation;

Overall inflationary pressures have increased;

Further tightening may be required;

Lack of downward momentum in inflation is a concern;

They remain data dependent; and

Rates needed to remain higher for longer.

All pretty hawkish as, inflation fearing rhetoric. Rogers up later today so watch out for any further opining.

Central Bank Speakers

The ECB’s Kazaks emphasised that rates were kept steady to keep inflation falling and rate cuts will come once it is clear that inflation is beaten. However the possibility of further rate increases cannot be excluded.

Makhlouf admitted that it was too early to declare that we have reached the top of the ladder of interest rates. Too early to discuss interest rate cuts.

Wunsch claimed that it was now less likely that the ECB need to raise again.

Lane stated that the ECB needs to make more progress on inflation.

Vujcic felt that the last mile in the inflation fight will be the hardest.

Nagel echoed those comments as he said that the last stretch before we reach our inflation target might well be the hardest. He also dismissed chatter on rate cuts as not helpful and much, much too early.

The Fed’s Cook said that the Fed must remain vigilant to potential shocks that could exacerbate global financial system vulnerabilities. A further slowdown in China could worsen financial stresses with possible international spillovers.

Jefferson pretty similar with if inflation expectations rise the Fed may need to respond. In addition high uncertainty may justify aggressive policy if inflation expectations threaten to become unanchored.

Harker claimed he supported the steady stance of the last FOMC meeting and felt that now was the time to take stock of past rate hikes. Higher for longer with no sign of near term rate cuts. Labour market is becoming better balanced with inflation falling to 3% next year.

The BoE’s Bailey was very forthright claiming that policy is now restrictive and economic growth is very subdued but policy will need to be restrictive for an extended period. Too early to be talking about rate cuts. Optimistic that 2% target will be met in a two year horizon.

BoJ’s Suzuki claimed that the Bank sees June next year as a critical time where Japan can see inflation adjusted wages turning positive.

Ueda meanwhile insisted that the BoJ will continue the easy policy to help wage growth. In the longer run labour productivity growth can help to push up real wages. Furthermore he claimed that monetary policy can help raise wages via tighter labour market by keeping real interest rates low and hence stimulating the economy. When asked directly what would be needed to end YCC and negative rates he responded that confirmation of the pass through of import prices had dissipated and whether wage inflation cycle kicks off as they expect.

He said this morning that companies were becoming more active than previously raising prices and wages. This adds to his conviction that Japan was making progress towards sustainably hitting its inflation target.

PBoC comments yesterday garnered some attention; China faces challenges from a slowing economic drivers including property, infrastructure and exports. It is in the middle of a 5% medium speed growth which may last another 5/10 years. China needs to continue to maintain a relatively loose monetary and fiscal policy.

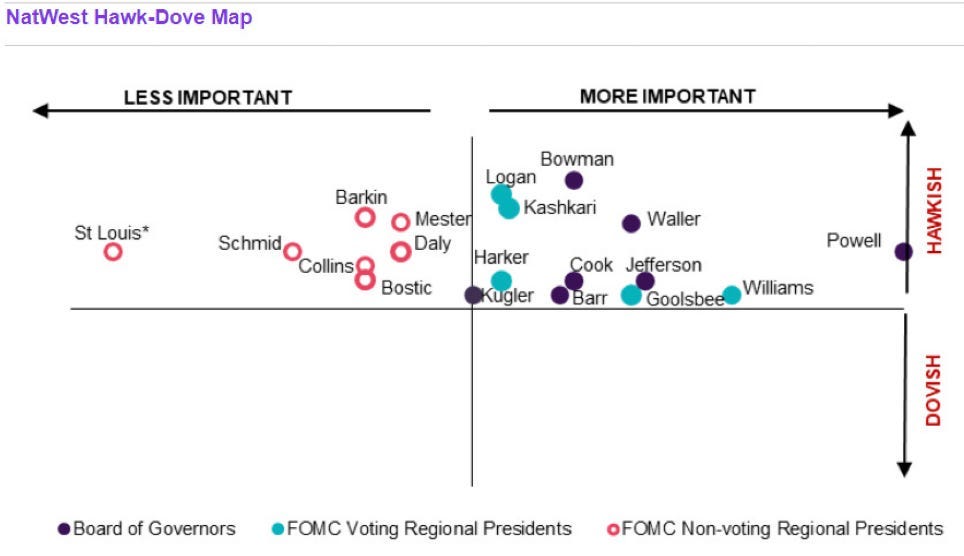

Once again the Fed map for reference.

The Day Ahead

Overnight October China’s inflation report showed both measures in deflationary territory. The MoM registered at -0.1% which brought the YoY for October to -0.2%.

Later in the day a smorgasbord of central bankers from around the world with the BoJ, Norges, BoC and SNB all getting involved on top of the usual ECB, BoE and Fed speakers. Ueda, Lagarde and Powell (if he can be bothered) probably take top billing.

Overnight the RBA minutes and then early doors tomorrow we have, what could be, the pivotal Norwegian inflation report and the UK data dump.

👍 If you found this morning’s briefing helpful, please consider giving it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience.

Follow the latest market narratives through our curated research & commentary channels on Harkster.com

Main Highlights Ahead

All times in GMT (EST+5 / CET-1 / JST-9)

The main highlights for the day ahead in terms of data and speakers:

Thursday

BoJ Ueda speaks (08.35 GMT)

Norges Bank Governor Bache Speaks (14.00 GMT)

BoC Rogers Speaks (17.00 GMT)

SNB Schlegel Speaks (17.15 GMT)

SNB Moser Speaks (20.30 GMT)

Fed Speakers

Bostic (14.30 GMT)

Barkin (16.00 GMT)

Powell (19.00 GMT)

ECB Speakers

Lane (08.10 GMT)

Lagarde (17.30 GMT)

Early Friday

RBA Statement on Monetary Policy (00.30 GMT)

Norway Inflation Rate MoM Oct consensus 0.6% vs previous -0.1% (07.00 GMT)

Norway Inflation Rate YoY Oct consensus 3.6% vs previous 3.3% (07.00 GMT)

Norway Core Inflation Rate MoM Oct consensus 0.3% vs previous 0.4% (07.00 GMT)

Norway Core Inflation Rate YoY Oct consensus 5.6% vs previous 5.7% (07.00 GMT)

UK GDP QoQ Prel q3 consensus -0.1% vs previous 0.2% (07.00 GMT)

UK GDP YoY Prel q3 consensus 0.5% vs previous 0.6% (07.00 GMT)

UK GDP MoM Sept consensus 0% vs previous 0.2% (07.00 GMT)

UK GDP YoY Sept consensus 1% vs previous 0.5% (07.00 GMT)

UK Industrial Production MoM Sept consensus 0.1% vs previous -0.7% (07.00 GMT)

UK Industrial Production YoY Sept consensus 1.1% vs previous 1.3% (07.00 GMT)

UK Manufacturing Production MoM Sept consensus 0.3% vs previous -0.8% (07.00 GMT)

UK Manufacturing Production YoY Sept consensus 3.1% vs previous 2.8% (07.00 GMT)

Good luck.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

My go to every morning - TY and dont disappear again please !!