The Morning Hark - 10 Nov 2023

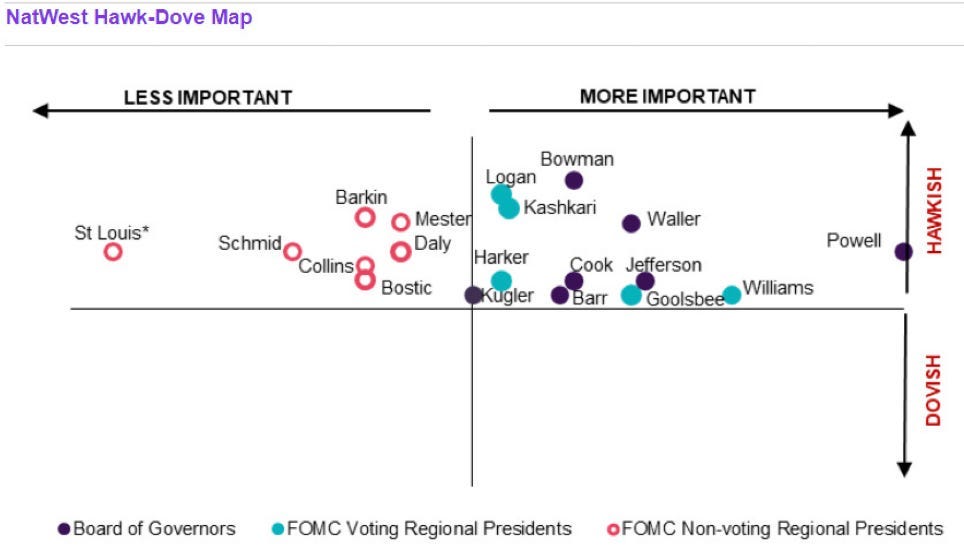

Today’s focus...Powell’s Dirty Harry moment on rates, spoos and protestors. Anyone else central bankered out? And for one last time (for now) Nigel Farage’s favourite bank’s map.

Please note that the Harkster Research Platform had some technical upgrades over the weekend. You may need to hard refresh your browser tab or re-download your Harkster iOS app for the platform to work correctly. See here for more details.

Overnight Highlights

Prices are at 6.25 GMT/1.25 EST, with changes reflecting movement from midnight GMT

Oil - Brent and Crude January futures once again finding a touch of support in Asia. The pair currently sitting up a touch at 80.40 and 76.10 respectively. Despite the small support in Asia its looking like a third week of losses for the sector as the Middle East tensions premium seems long gone and the weaker global demand story gets more legs. In addition Powell’s hawkish stance did little to help.

EQ - Asian equity markets mixed overnight with Powell’s hawkish comments leading the Hang Seng lower by close to one percent at 17,255. The Nikkei fairing a bit better currently flat at 32,580.

The US indicies flat in Asia but holding onto the majority of their recent gains with the Nasdaq and S&P futures at 15,245 and 4365 respectively. The S&P winning streak was sadly taken away by Jay.

Gold - Gold Dec flatlining in Asia currently at 1961 as the safe haven trade continues to look a distant memory.

FI - Global yields softer in Asia trimming some of the gains post Powell. The US2y and US10y currently trading at 5.02% and 4.62% respectively.

One point of note was the US 30y auction which had the biggest tail on record. More details below in the ING article.

German 10y yields closing little changed at 2.65% and the Italian 10y yield similarly at 4.52%.

UK gilt yields likewise with it closing at 4.27%.

FX - USD flat and holding onto its post Powell gains with the USD Index currently at 105.90. The JPY, EUR and GBP all a touch lower than previously versus the USD currently at 151.40, 1.0670 and 1.2225respectively.

Others - Bitcoin and Ethereum up overnight. Bitcoin a touch stronger at 36,620. Ethereum however up close to ten percent at 2110 with the Blackrock news.

Blackrock is growing in confidence that the SEC will approve a Bitcoin ETF by January. In addition they are eyeing up an Ethereum ETF too as they have deemed to have registered a vehicle in Delaware for such a product.

Macro Themes At Play

Powell Recap

Powell, in the face of climate protesters, has his Dirty Harry moment

THE MONEY LINE…….”JUST CLOSE THE FCKG DOOR”.

I wish I could end it there but he actually did say some other things of interest.

Moneylines

Not confident we’ve achieved sufficiently restrictive stance;

But on the other hand……we probably have significantly restrictive policy;

Will not hesitate if tightening further becomes appropriate;

Biggest mistake would be to fail to control inflation;

Attentive to the risk that stronger growth could undermine inflation progress which could warrant monetary policy response;

While the broader supply recovery continues, it is not clear how much more will be achieved by additional supply side improvements;

A greater share of progress on inflation ahead may have to come from tight monetary policy, not just supply side improvement;

We will continue to move carefully, and move meeting by meeting; and

Again what has been a theme of the week and they are still looking for answers I guess……we’re looking carefully at reasons behind recent yield surge.

Timiraos the WSJ Fed whisperer’s take on it all was that despite the hawkish tone he did little to lay the groundwork for a December hike, they will remain on hold but that doesn’t mean rates can’t move higher again in early 2024.

From our point of view the majority of the Fed speakers this week have been along these Powell lines but Powell, whilst obviously being the main voice, was also the most succinct and forthright in those views. We did think there would be some pushback on the market’s move since last week’s presser and NFP print but it does beg a couple of questions. If long term rate yields hadn’t sold off 60bps would he have been this hawkish? I doubt it. Secondly did he really think that after his presser the market wouldn’t sell off aggressively given the over extended nature of it? Harry hindsight I know but surely he’s been round long enough. Anyway…..everyone over the other side of the boat!

Back to the market reaction. As you’d expect USD better bid, yields spiked and equities took a bath. As we thought he might, he did break the Spoos winning streak but when we step back and look at the bigger picture the USD and US yields are lower than when he stood up post FOMC and equities remain higher. Rate cut wise expectations have been pushed back again to June of next year from May previously.

Central Bank Speakers

The ECB’s de Guindos suggested that leading indicators point to a growth outlook being somewhat negative than we had previously projected but rate cuts wise we are not there yet. I see risks for the inflation outlook in the next months.

Villeroy insisted that rates will not go up without external shocks. Inflation is clearly trending downwards.

Vujcic felt that the ECB must be ready for either rate hikes or cuts next year although its too early to consider rate cuts just now.

Centeno seemed to think that the ECB was at a plateau interns of interest rates. Monetary policy is working which is helping inflation to come down.

The Fed’s Goolsbee noted that the Fed will need to watch for risks of overshooting on rates. Higher long term rates can have a substantial effect if sustained. Too soon for the Fed to consider rate cuts.

Barkin continued the hawkish theme by claiming that it remains to be seen if more tightening is needed especially as inflation will be more stubborn than recent data suggests. Echoing Powell later in the day he stated that he has a hard time declaring sufficiently restrictive at any point in time. There is still tightening to come, more lag to come for hikes so far.

On long term rates he does not view them as a policy variable.

However he believes a slowdown is coming which will help in getting inflation lower.

Bowman still expects to see further rate hikes.

Bostic was certain that the Fed would remain restrictive until the 2% inflation target was met. Unlike Messers Barkin, Bowman and Powell he felt that policy was sufficiently restrictive.

Paese saw the path back to 2% inflation as bumpy and it is unclear whether tighter financial conditions will provide needed restraint. She however did back the pause in rates.

The BoE’s Pill reinstated his view that inflation remains much too high but policy tightening is now “bearing down” on it but it is still not a time for complacency. However he felt there was no need to raise rates but he assumes that rates will stay restrictive for an extensive period. However if the economic situation changes the BoE will need to change policy. He did note that developments in the real economy are weaker than forecast.

BoJ’s Ueda urged caution as the central bank moves to raising interest rates. He felt that the wage-inflation cycle is slowly rising but there remains a lot of uncertainty on inflation. Like Suzuki yesterday he was keen to emphasis the spring wage talks next year.

He also wanted FX to reflect fundamentals……hate to break the news but……

Norges Bank’s Bache was clear that the bank does not have a policy target for the Krone.

The BoC’s Rogers was begging up the Bank’s policy by claiming that adjusting early and bit by bit to higher rates lowers risks of having to take more abrupt and potentially destabilising steps later. The Bank is not yet talking about rate cuts and people should expect higher rates in the long run than previously.

Given the number of Fed speakers, for one last time, (for now) the map courtesy of NatWest…they do do some things well Mr Farage!

The Day Ahead

Overnight the RBA’s Statement on Monetary Policy showed risks of upside surprises for inflation within their outlook. A pause was considered before voting for a hike but risks remain that inflation will take longer to return to target.

Forecast wise, based on 4.5% rates, inflation (4% by June 24 from 3.25%) and GDP (1.75% by June 24 from 1.25%) raised whilst unemployment and wage growth were cut smalls.

Early morning we get the potentially pivotal Norwegian inflation report for October and the UK data dump with the prel q3 GDP reading being the highlight.

Later in the day the UMich prel November survey with the all important inflation expectations and a dwindling band of central bankers; Lagarde probably takes top billing.

👍 If you found this morning’s briefing helpful, please consider giving it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience.

Follow the latest market narratives through our curated research & commentary channels on Harkster.com

Main Highlights Ahead

All times in GMT (EST+5 / CET-1 / JST-9)

The main highlights for the day ahead in terms of data and speakers:

Friday

Norway Inflation Rate MoM Oct consensus 0.6% vs previous -0.1% (07.00 GMT)

Norway Inflation Rate YoY Oct consensus 3.6% vs previous 3.3% (07.00 GMT)

Norway Core Inflation Rate MoM Oct consensus 0.3% vs previous 0.4% (07.00 GMT)

Norway Core Inflation Rate YoY Oct consensus 5.6% vs previous 5.7% (07.00 GMT)

UK GDP QoQ Prel q3 consensus -0.1% vs previous 0.2% (07.00 GMT)

UK GDP YoY Prel q3 consensus 0.5% vs previous 0.6% (07.00 GMT)

UK GDP MoM Sept consensus 0% vs previous 0.2% (07.00 GMT)

UK GDP YoY Sept consensus 1% vs previous 0.5% (07.00 GMT)

UK Industrial Production MoM Sept consensus 0.1% vs previous -0.7% (07.00 GMT)

UK Industrial Production YoY Sept consensus 1.1% vs previous 1.3% (07.00 GMT)

UK Manufacturing Production MoM Sept consensus 0.3% vs previous -0.8% (07.00 GMT)

UK Manufacturing Production YoY Sept consensus 3.1% vs previous 2.8% (07.00 GMT)

US Michigan Consumer Sentiment Prel Nov consensus 63.7 vs previous 63.8 (15.00 GMT)

US Michigan Inflation Expectations Prel Nov consensus % vs previous 4.2% (15.00 GMT)

US Michigan Inflation Expectations 5y Prel Nov consensus % vs previous 3% (15.00 GMT)

Fed Speakers

Logan(12.30 GMT)

Bostic (14.00 GMT)

ECB Speakers

Lagarde (12.30 GMT)

Good luck and a good weekend to one and all.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

2024 another bad year ???

Maybe 2025 or 2026 will be good......

Yes, CBed out, definitely.....