The Weekly Hark - 17 June 2023

Soft Landing

As has been customary over the past few weeks, markets have once again rallied into the weekend. The combination of softer PBoC/BoJ policy and the June Fed SEP projecting a soft landing has emboldened sentiment and taken ESA into Bull market territory as the market is under-invested. Performance post-Friday’s quarterly Opex will be closely watched in the major indices, but sentiment is most certainly tilted towards a FOMO rally ... is there anything that can deter the momentum as we head deeper into the summer doldrums?

Asian CB’s are still expanding their balance sheet... BoJ normalization pushed deeper into the future as they forecast CPI returning sub 2% whilst PBoC continues to ease domestic rates and target direct lending into countryside infrastructure builds and the EV market. The liquidity push in Asia is going someway to offset the balance sheet unwinding in Europe and the US. Furthermore, expectations are growing of a large fiscal push from China which fed into commodity prices and supported a rebound in HSI, Copper, Oil etc over the past few weeks.

Fed skipping not pausing and projecting a soft landing.... higher 2023 growth, stickier inflation and a stronger labour market dropping their end of yr UER down from 4.5% to 4.1%. Crucially the Fed no longer sees a recession in 2023 but is happy with the pace of inflation returning back towards target in the forecast horizon. Either the economic cycle will turn south, or more hiking will be required (#Higherforlonger), but after 500bps of hikes, they’re happy to be #datadependent going forward.

Summer has arrived early in vol markets... CVIX @ 7, VIX < 14 ... models are thus gorging on carry as a result.

After the AI halo insulated the market from real rates / CRE fears in H1, now a broadening of market performance may induce a FOMO rally. Performance will be bolstered by investors comfortable in the knowledge that the Fed is close to being done, earnings recession is sliding into 2024, and bank credit lending remains consistent. The market has had bubbles before, with Fed rates around 5%.

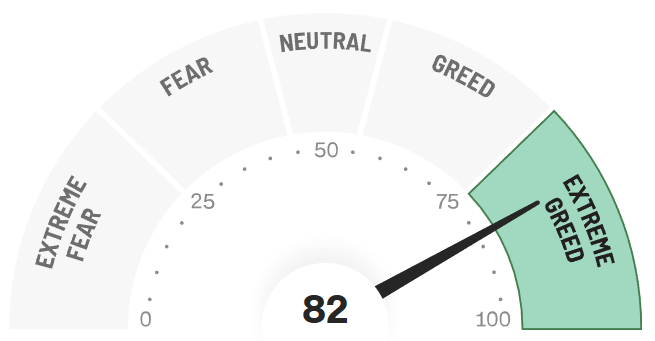

CNN's Fear and Greed Index @ 82 ... as the recessionary clouds lift from the horizon, who can argue with a market chasing performance. However, as consensus sits comfortably in the high beta, high return world, what is the unknown unknown that can trigger a position unwind?

The key pieces capturing last week’s driving narratives

BCA Podcast: Global Central Bank Round-Up

Mauldin Economics: A Skip, Not a Stop

Joseph Politano: Tepid Optimism for a Soft Landing

The Gryning Times: Unanimity

Kyla Scanlon: Preserving Optionality and Other Things

Charles Schwab: 2023 Mid-Year Outlook: U.S. Stocks and Economy

The Macro Compass: Jawboning

Eurodollar University: Conflicted Fed stuck btw rapidly disappearing inflation & bank crisis already reappearing.

Econostream Media: Market Reaction to ECB Decisions ‘Seems Somewhat Excessive’, Villeroy Says

Saxo Bank: Crude oil rises on upbeat demand outlook and China stimulus focus

11 Fed speakers including JPow, BoE, Norges and SNB

Adam Mancini: After A 100 Point Squeeze, Is It Finally Time For SPX To Pullback?

Scotiabank: The Global Week Ahead: Supply Chain Fairy Tales

Given the complexity of modern-day finance, as multiple narratives fight for supremacy .... the simplicity, insightful and comprehensive summary of the day’s best charts delivered by the

is greatly appreciated by Harkster HQ. The curation really does deliver on the old adage that “A picture is worth a thousand words”. It curates and blends a fantastic array of cross-section macro and market data.

Follow in the Harkster ‘Feed of the Week’ channel.

CNN Fear and Greed hit’s 82

Source: Fear and Greed Index - Investor Sentiment | CNN

If you enjoyed this week’s newsletter, please give it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience 🙏

Follow the evolving market narratives through our curated research & commentary channels on Harkster.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

Thanks for the shoutout and the kind words! Have a great weekend!

Nice overview