The Saturday Hark Back - 30 Sept 2023

Capturing the themes of the week when there’s more time to digest them.

The key narratives that drove markets last week:

With little top tier data on the docket last week, the yield move that commenced post Fed ran out of a little steam, became a little too consensus and most likely ran into some rebalancing flows as month end is normally a good time for duration. As a result, we ended the week with the "USD up, Yields up, Equities down" camp on the backfoot and feeling a squeeze for the first time since JPow unleashed the revised 2024 dots on the market. In particular the USD high came just after the Corp t+2 session ended on Wednesday afternoon/evening and we spent the rest of the week with a softer DXY.

We may not have had a lot of data, but there was most certainly a lot to discuss as Biden/Trump went to woo Michigan union workers and the electorate (WSJ), UAW strikes are expanding, but are EVs killing jobs (Rep Senate candidate Mike Rogers), Housing market in the US finally started to creek under the weight of mortgage yields not seen for over a decade, the steepening of the curve has the sell /buy side focused on 5% (Bloomberg), the search for the next SVB / hidden leverage in the system is once again turning towards Private Equity (Private Equity Investors Face Expensive Choice: 10% Loans to Get Cash) and of course we all became basis "experts" for an afternoon as the FT reports regulator worries around the leverage in the UST trade. Most importantly with the US government shutdown now upon us and McCarthy fighting to maintain his speakership, the data dependent Fed has no data to react too (WSJ).

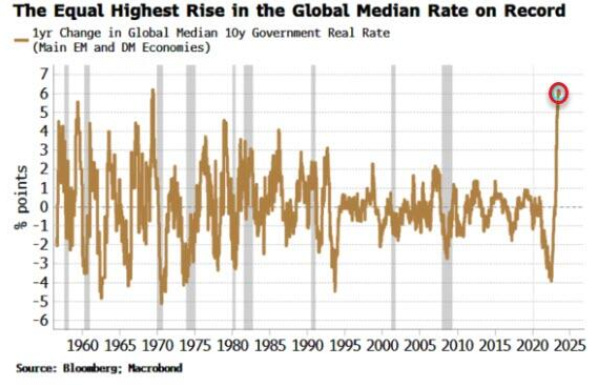

In hindsight, there is a laundry list of reasons for why duration is selling off... QT, convexity hedging, primary dealers have limited room to take down more paper as hold to maturity losses mount, Bidenomics / deficit explosion, Fed on the path to forecasting a higher neutral rate, BoJ dampener removed (Bloomberg: biggest sell off in 25yrs hitting Japanese bonds), a US economy that simply will not die as households and corps are insulated having refinanced at ultra-low post covid rates, Treasury issuance exceeding expectations, China with fewer USD to park in UST (for political reasons or maybe just because their surplus is shrinking and they're selling USD to support the Yuan), US shutdown / Moody's downgrade comments, with oil soaring, Fed locked in on not doing much more, the only thing left to move is the long end, especially as the market is caught invested in the recession theme etc etc....

…. but a word of warning from Simon White (Bloomberg)... We may hit 5%, but nothing goes in a straight line and the location of the short duration trade is far from ideal as we've just seen one of the largest sell offs on record... With mortgage rates finally starting to weigh on the US housing market, will the economy follow? (Barclays: Are US house prices set to fall?) .... Duration needs a recession but at least there are continued signs of disinflation from Tokyo to Europe and the Fed's PCE ...

Bearish equity sentiment is also running into extremely positive October Seasonals, core positions are now left directionless as China goes on holidays with vol naturally expected to die whilst furloughed government departments will not be releasing the all-important data needed for us to price the probability of a Nov hike.

ㅤ

Top 10 Reads of the Week on Harkster.com :

Brent Donnelly: Friday Speedrun

Steno Research: EUR INFLATION WATCH: ANOTHER COUPLE OF MONTHS OF EASY DISINFLATION ON THE CARDS

Bloomberg: China’s Economy Improves in September, Satellite Data Show

Brent Donnelly: One Less Vulnerability

Ashenden Finance: The soft-landing narrative is fading, together with the market bullishness

Man Group: Views from the floor - Macro Signals Suggest Risk-On Continues

Doomberg: The Great Backpedalling Is Upon Us

Wealth of common sense: Where the Housing Bubbles Are

Capital Flows and Asset Markets Should I Short Private Equity

The majority of these links appear in our new "HarksterPro - Intraday Market Colour" channel. If you click on "Select Channels", you should find under "Added Recently" our latest additions to the app. @HarksterHQ will use this new channel to flag good articles/sources of content as well as headlines/market moving events.

Top 5 Podcasts of the Week:

JPM Global Data Pod Weekender: Rising yields meet resilience growth

JPM Global FX: Dollar strength moves up a gear

MacroVoices: Simon White - Inflation, Stocks & Why TINA is Coming Back

Forward Guidance: Luke Gormen - Panic In The Bond Market Will Continue Unless Oil Or Dollar Relent

Looking forward to next week...

ING Economics: Key events in developed markets next week

The Global Week Ahead: Shutting Down

S&P Global: Week Ahead Economic Preview: Week of 2 October 2023

We would like to thank the

author for pointing us in the direction of some excellent new content feeds ... As always, if there is anything you would like added to the library pls get in touch with hello@harkster.com, in the comments below or message @HarksterHQ on

If you enjoyed this week’s newsletter, please give it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience 🙏

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

Thanks for mentioning our work. We appreciate the vote of confidence!