The Saturday Hark Back - 25 Nov 2023

Capturing the themes of the week when there’s more time to digest them.

The Hark Back

The key narratives that drove markets last week:

A holiday disrupted week, with limited top tier US data and Fed speak leaving us in a natural holding pattern. Traders globally took the opportunity to take time away from the desk, re-energise their batteries ahead of the final push, just 3 maybe 4 weeks of real trading conditions left for the year.

There has been plenty to occupy the mind from RoW but nothing to override the bubbling expectations of a mild US recession in 2024 (more below). Hunt's Autumn statement cut taxes for workers and corps (FT - Hunt gambles fiscal tailwind on voter-friendly tax cuts), Opec+ output cut was delayed until Nov 30th as members struggled to agree quota's, Altman's exit/return dominated the US press (Understanding AI - Firing Sam Altman hasn't worked out for OpenAI's board), Nvidia earnings beat lofty expectations but forecasted exports to China remain a concern as Biden's regulations bite, Gaza/Israel commenced a 4-day truce, Riksbank failed to hike (Riksbank review: On hold - peak policy rate), ECB speakers indicated rates are restrictive / at peak (Econostream - They Said It: Recent Comments of ECB Governing Council Members).... but the ultimate focus has been on the cost of Turkey and food inflation, which Biden will have to fight against on the campaign trail (ZeroHedge - A Traditional Thanksgiving Turkey Dinner Is 30% More Expensive Since Biden Took Office) and subdued consumer demand on black Friday as covid spending dwindles and credit tightens (Black Friday Finds Picky US Shoppers Waiting for Bigger Bargains).

A natural bias of short USD, long equities has formed as Fixed Income vol dissipates (10s settles around 4.40%) and the strong seasonals take hold. The RoW is getting a perceived boost from the "hope" of a targeted round of Chinese stimulus and support for their most maligned property companies (Bloomberg - China Weighs Unprecedented Builder Support With First-Ever Unsecured Loans) and German Ifo is showing signs of stabilisation. The trend of the US economy catching down (Apollo Academy - Youth Unemployment Rising Quickly) with the RoW persists (or maybe the narrative is just chasing price action).

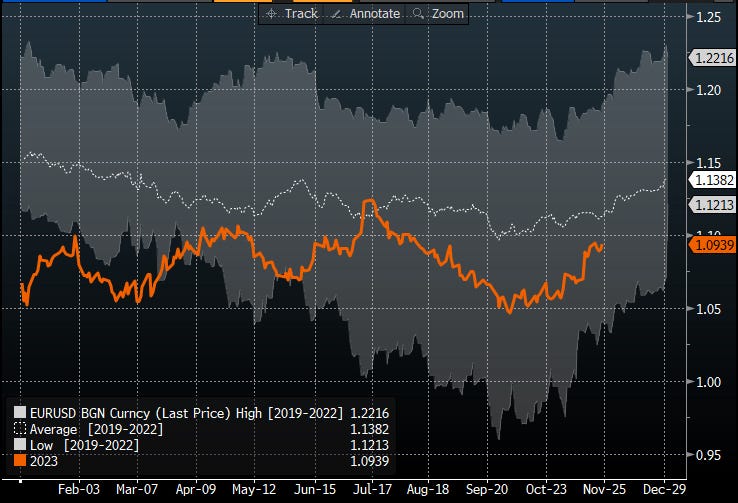

2023 in FX has been particularly disappointing. Equities have had their Mag 7 / AI boom (Reuters - HEDGE FLOW 'Magnificent 7' bets drive hedge fund crowding to record high -Goldman Sachs), bond vigilantes have had their day in the sun in FI markets, but the ranges and natural dispersion within FX has been particularly disappointing relative to the spoils of 2020, 2021 and 2022. As the Bloomberg chart below shows, EURUSD 2023 range (orange) pales in comparison to those seen during covid lockdowns, the grand reopening and of course the Ukraine / Russia war and subsequent European energy crisis. Maybe we're asking too much for a material Dec year end trend.

Source Bloomberg

Themes forming in the 2024 preview ...

Consensus is now firmly expecting a US soft landing which leads to peak rates and bonds offering an attractive return.

BoJ normalization, tightening more than expected, higher wage agreements, add in a US recession and USDJPY to trend lower (i'm pretty sure I wrote this in Oct/Nov 2022... but let's try it again)

Maturity wall finally strikes - countries (GBP/CAD) and companies (CRE tsunami) with high sensitivity to refinancing rates will underperform

2024 is the year of the election with 40 national elections scheduled (Bloomberg)

This week is a microcosm of what is to come. In the UK BoE's Bailey has been pushing back against market pricing of 2024 cuts, repeating the higher for longer mantra and refreshing the warning that he will do more if inflation re-engages. However, on the other side of the ledger, Sunak in No.10 has been claiming victory on the government's target to reduce inflation by half this year (I didn't know he could control base effects or energy markets) and Hunt has delivered a wave of Tax cuts, giving away the unexpected 20bln he had in the coffers. Rather than saving it for a rainy day, he answered the wishes of the right of the party and cut National Ins and rolled out some incentives/savings for Corporates.

FiveThirtyEight - If The 2024 Election Were Held Today, Would Trump Win?

De-globalisation and onshoring... MXN > CNH

Europe the first to head into recession (but How Well Do Economists Forecast Recessions? ... IMF working Paper)

ETF regulatory sign off for Bitcoin and Ethereum

Equities to be in-line to higher... The AI productivity gains and deflationary forces offset the burden of higher real rates on corps and softer lending to households. (BofA - The Bull Case for US Stocks)

These themes can define allocations and flows for the next 2months (Dec into Jan) but rarely hold true for the full year (ZeroHedge - "Only Conviction For 2024 Is Market Consensus Won't Equal Success")

10 pieces from our dedicated Year Ahead channel on Harkster.com...

HFI Research - A Realistic Look At The Oil Market Balance In 2024

ING - Rates Outlook 2024: The big US fiscal deficit and effect on market rates

Oxford Economics - Global Macroeconomic Themes 2024: Few opportunities in a gloomy landscape

Morgan Stanley - Ellen Zentner: 2024 U.S. Economic Outlook

Goldman Sachs - Why the global economy and markets can continue to outperform in 2024

ING - 3 Key FX themes for 2024

Top 10 Reads of the Week on Harkster.com:

Telegraph - Winners and losers of Jeremy Hunt’s 2023 Autumn Statement

Steno Research - USD’o’meter: Is King USD about to reverse?

Man Institue - Trend-Following and Long/Short Quality: Attack Wins You Games, Defence Wins You Titles

Macro Hive - Charts of the Week: Time to Buy Bonds?

Politico - How a billionaire-backed network of AI advisers took over Washington

FT - Emerging economies deserve praise for their monetary policy moves

NY Fed / Liberty Street Economics - What if the Fed had stuck to AIT Rule?

Capital Flows and Asset Markets by Russell Clark - PRO-LABOUR POLITICS AT WORK

Axios -The subscription economy

The MacroTourist - WATCH FOR A SUBTLE FED SHIFT

The majority of these links appear in our new "HarksterPro - Intraday Market Colour" channel. If you click on "Select Channels", you should find under "Added Recently" our latest additions to the app. @HarksterHQ will use this new channel to flag good articles/sources of content as well as headlines/market moving events.

Top 5 Podcasts of the Week:

Animal Spirits Podcast - You Can't Quantify Happiness - A Wealth of Common Sense

Unchained podcast - Binance's Historic Settlement: What You Should Know

Schroders - The Value Perspective with Jamie Lowry and Ian Kelly

BofA - A real boost to operating margins through artificial intelligence

Forward Guidance - Jens Nordvig: Interest Rates Have Peaked, The U.S. Dollar Is Overvalued

The Week Ahead

Scotiabank - The Global Week Ahead: Markets Need A Little Holiday Cheer Global Week Ahead November 24, 2023 Derek Holt

If you enjoyed this week’s newsletter, please give it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience 🙏

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

BoJ normalization, tightening more than expected, higher wage agreements, add in a US recession and USDJPY to trend lower (i'm pretty sure I wrote this in Oct/Nov 2022... but let's try it again)

don't worry, you'll get to write it again next year!

🤣🤣🤣🤣....