The Saturday Hark Back - 13 Apr 2024

Capturing the themes of the week when there’s more time to digest them.

The Hark Back

The key narratives that drove markets last week:

Theme 1 - Inflation closes the Fed's cutting window before the election

Theme 2 - Economists mark to market Fed expectations

Theme 3 - Israel/Iran on the edge of a precipice

Theme 4 - Commodities / USD correlation breakdown

Theme 5 - Soft start to earning season

Theme 6 - ECB ready to cut

Theme 7 - AI dominates the headlines

Theme 8 - On the campaign trail

Theme 9 - China

Top 10 Reads of the Week on Harkster.com

Top 5 Podcasts of the Week

Week Ahead Preview

Theme 1 - Inflation closes the Fed's cutting window before the election

Even when it was first mentioned by Powell, there was a pocket of market participants that queried if the Fed's Dec pivot was too soon, and could potentially inflame inflation at the wrong part of the cycle. After 3 hotter prints, a strong economy as gdp growth chuggs along around 2/3% and of course a resilient labour market, the disinflation trend has clearly stalled.

Jamie Dimon told us earlier this week that the soft landing was in question (WSJ - Jamie Dimon Warns U.S. Might Face Interest-Rate Spike). Given JPM's data insight and view into the financial piping of US corporates and households, it pays to listen. Although @EpsilonTheory has been highlighing the lack of momentum in the disinflation trend for 9months. Along with the more recent rise in commodities, the expected rise in food prices ... the job is most certainly not done for the Fed.

Rightly or wrongly, 4.5% has been named in many a piece as a "trigger" level, a risk level for fixed income moves to finally feed into VAR models and encoruage/expediate equity derisking. The 3bps tail for the 10year auction as well as the weak 30year auction will also worry investors and encourage bond vigilantes to reappear on FinTwit after their Q1 hibernation.

Source: @EpsilonTheory

Where does this leave the Fed? If they don't cut in June, the POTUS election complicates the arthematic

The following was first published by my colleague in The Morning Hark - Apr 09,...

"We have 6 FOMC meetings left for the year: May, June, July, September, November, December.

The under/over is around 3 cuts for the year although Fed chatter is diluting these at every turn!

The FT quoted Bespoke Investment Group’s study on US election year Fed moves and found that in election years the Fed held steady at 71% of their meetings as opposed to 67% in other years. If that is narrowed down to the more sensitive months of an election year between May and November the numbers become even more diverse at 81% versus 65%. If we only talk about rate cuts, within those months, then the Fed has cut rates at only 3% of those meetings as opposed to 14% in other years.

We can take May out straight away so that leaves 5 meetings and if the above stats are to be repeated its a long call that we get any cuts between June - November which leaves a December Santa rate cut just in time for the year end rally!"

ZeroHedge - The Case For Owning Treasuries Is Evaporating

Yardeni Research - The Last Mile

NY Times - Housing Costs Continued to Rise Faster than Before the Pandemic

The Inflation Guy - This Month's CPI Report - A Potential Pony Situation

Advisor Perspectives - Inflation Since 1872: A Long-Term Look at the CPI

Steno Research - US CPI REVIEW: INFLATION IS ACCELERATING, NO RETURN TO 2% IN SIGHT

The Boock Report - 10 yr auction was bad

The Next Economy - Second Wave or Bump in the Road?

ZeroHedge - Ugly 30Y Auction Tails For First Time Since November, Lowest Foreign Demand Of 2024

CreditNews - The hidden reason inflation is stuck

Steno Research - US CPI REVIEW: INFLATION IS ACCELERATING, NO RETURN TO 2% IN SIGHT

Theme 2 - Economists mark to market Fed expectations

The US economy simply does not need rate cuts given the strong labour market, easy financial conditions, wealth effect from the AI fuelled equity rally, the 5.25% coupon the US Treasury now pay savers, the last mile of disinflation stalling, 3 hot inflation prints in a row, rise in commodity prices and heightened freight costs. For example, DB have felt the need to reevaluate their Fed view. "As we discussed in our recent note (see "(Pushed) Back to December") we now expect only one rate cut this year, at the December FOMC meeting followed by modest further reductions in 2025. A reduction in July is possible, though it likely requires a string of more favourable inflation prints than we currently forecast."

Source WSJ Nick Timarios

Barclays - Sept cut and 4 next year

The BondBeat - while WE slept

Bloomberg - First Fed Rate Cut Won’t Come Until December, Deutsche Bank Says

Steno Research - G3 Rates Watch: No one’s got a clue on R*, yet the market is convinced that it does!

Steno Research - Portfolio Watch: The USD wrecking ball is back

Brent Donnelly am/FX - Breakdowns

Reuters - Fed's Williams: Banks should be prepared to use discount window if needed

Even at 2 cuts, the Fed are still running things hot...

DB believe "a focus on 2024 cuts is too narrow. Risky assets remain robust because the market is still pricing 6 Fed cuts by the end of 2026, which is meaningfully more dovish than the Fed of last Summer and Fall. Risky assets are still benefitting from last November's Fed pivot, as the market has substituted fewer 2024 cuts with more 2025 cuts, especially post the US Presidential election"…

Source DB via The BondBeat

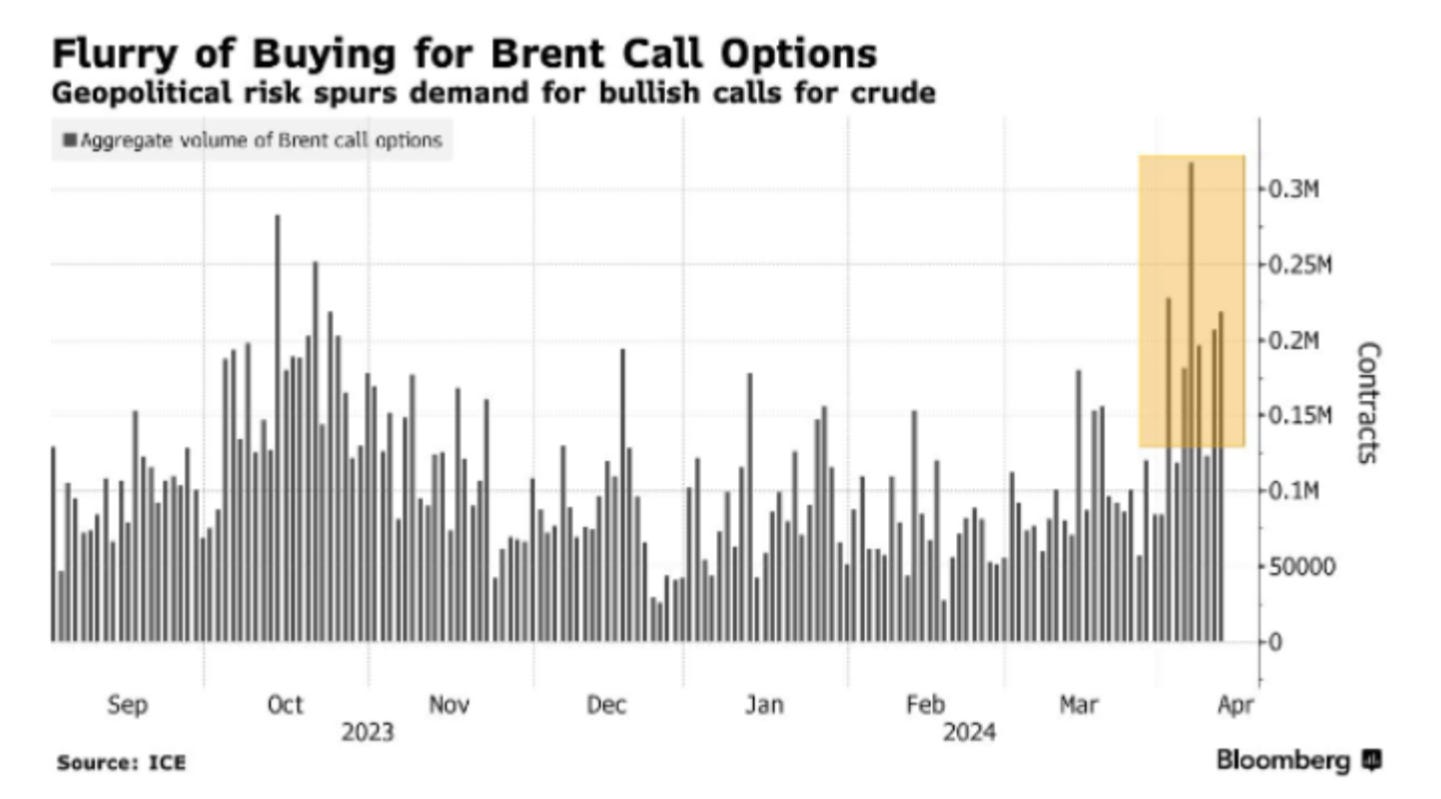

Theme 3 - Israel/Iran on the edge of a precipice

Ever since Biden warned of an imminent attack on Israel from Iran proxies, oil has squeezed to multi year highs and portfolio managers have increased call option demand, as potential hedges for other elements of their portfolio. Diplomatic channels are on overdrive as Biden sends his top regional General to Israel ahead of what could potentially be a devastating counter attack from Iran. Will they escalate, hit Israeli soil or will it be an "eye for an eye" strike, an Israel outpost. Expect the sabre rattling to continue through the weekend.

Source Bloomberg

Brent Donnelly (Friday Speedrun) summed it up nicely, how investors will managing their portfolio.... "There was angst going into last weekend about whether Iran might launch some kind of attack on Israel. We have had the same angst today. It’s a scary thing to think about, and I have no edge on attaching a probability to this possible escalation. But it needs to be on your radar for risk management reasons. Don’t wanna be short oil into the weekend, for example. If you can’t properly estimate your risk, it’s hard to manage it."

WSJ - U.S. Warns of Imminent Attack on Israeli Assets by Iran or Proxies

Steno Research - Israel-Iran War Coming?

Axios - U.S. aid official says famine has begun in northern Gaza

Axios - Senior U.S. general to visit Israel to coordinate on Iran attack threat

Axios - Iran signals it will limit response to Israel attack to avoid escalation

Theme 4 - Commodities / USD correlation breakdown

It took severe risk aversion on Friday as markets feared the worst of an attack on Israel by Iran to generate a speculative wash out in some commodities.

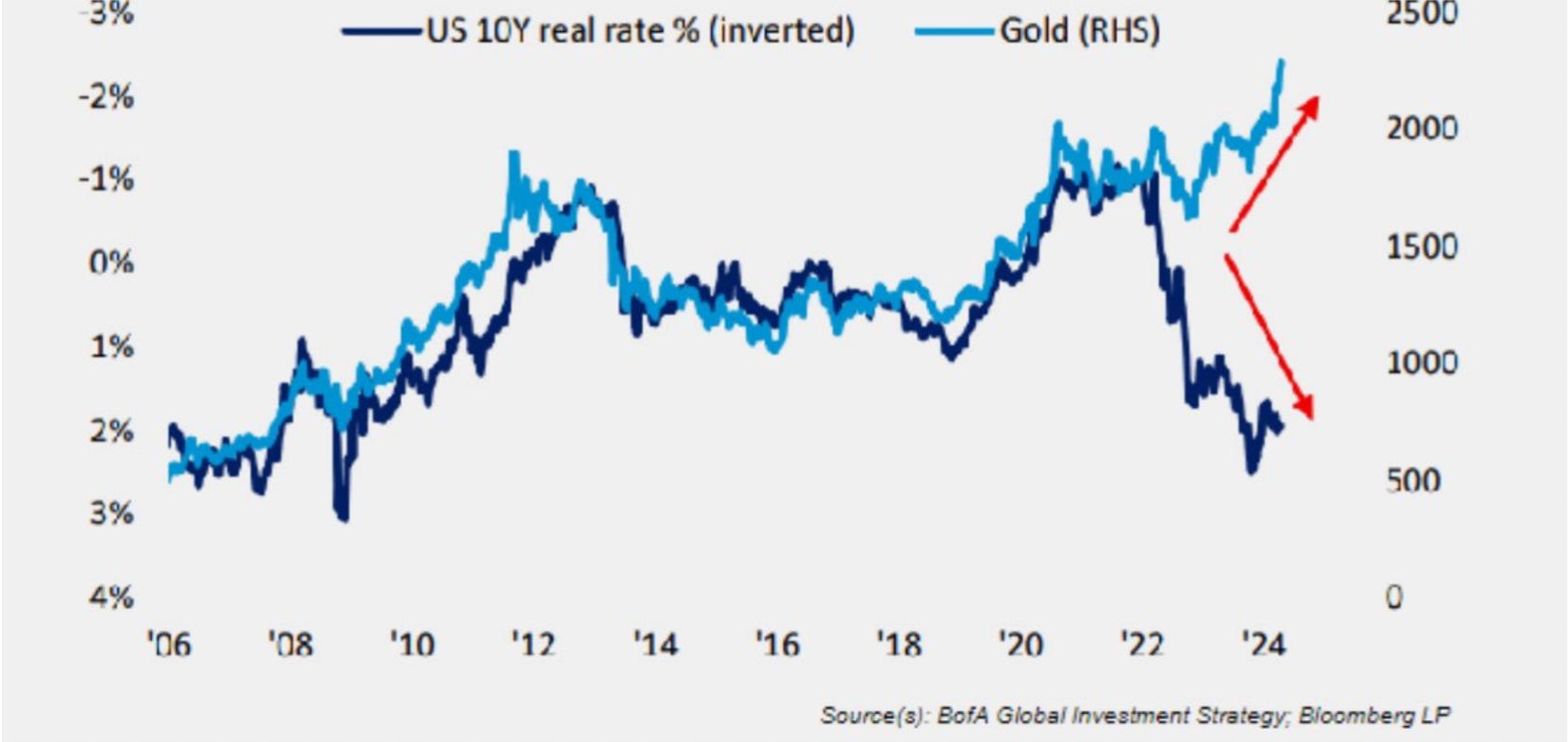

If tensions in the middle east ease, will the market go back into gold, silver, copper? The flows are there, momentum is strong and it's even more impressive to see commodities out perform as global assets reset to a limited 2024 Fed rate cutting path. Financial conditions remain easy, global manufacturing PMIs are turning around but the correlation breakdown between USD and metals is extremely rare and am sure has proved costly for many a PCA fair value trading model. Everyone is focused on CB flows as JPY and Yuan weaken relative to the USD, others are focused on retail from traditional buyers in India through to Costco selling gold bricks ... social media at work again as retail investors flock to Costco?

The broader commodity index (led by copper now at a 15month high) is being helped by the Chinese/US/German manufacturing turning higher, EV roll out, inflation hedge, wars (Ukraine vs Russia) and proxy wars (Israel vs Iran)... the reasons are a plenty, price action is engrossing as commodities offer momentum fundamentally lacking in FX, Equities and Fixed Income markets.

Rising copper/oil prices = higher food prices = higher rates of inflation = higher yields... It's too early for CB's to declare victory on inflation?

Explanations for the divergence of Gold and US real yields (Chart 1 source BofA) are landing firmly at the door of major CB's. If they stop buying will gravity take hold?

Source: BofA

Russell Clark - WHAT GOLD, REAL RATES AND GOLD MINERS ARE ALL TELLING YOU

WSJ - Gold Futures Hit New Record on Central Bank Buying, Safe-Haven Demand

Bloomberg - Copper Rally Continues With Surge to Highest in 22 Months

FT- Rio Tinto’s increasing copper exposure will add colour to its stock

The Macro Trading Floor - Yes, But What Will Break Markets?

NY Times - Gold Bar Sales Are Surging at Costco. Why?

FT - Record cocoa prices leave a bitter aftertaste for chocolatiers

MS Thoughts on the Market - What is Driving Big Moves in the Oil Market?

Bloomberg - Why Is Gold Suddenly Rising Right Now?

Steno Research - GOING GLOBAL AND REAL!

Bloomberg - Food Prices Are Up Under Biden, Like Every Other President

FT - Global oil market likely to be ‘extremely tight’, says Citadel

The Macro Trading Floor - The Next Big Trade?

Steno Research - Energy Cable: Melt UP in commodities upcoming?

Theme 5 - Soft start to earning season

The rise in US ISM normally projects to a rise in Q1 EPS (Source BofA via ISABELNET). This has yet to be seen with JPM profits rising 6% but their worrying outlook disappointing investors and leading to a heavy futures market on the NY open.

Saxo Bank - Q1 earnings season starts today

ISABELNET - U.S. ISM Manufacturing PMI vs. S&P 500 EPS Growth

FT - JPMorgan profits rise 6% despite $725mn regulatory charge

FT - Citigroup profits beat forecasts as bank sheds thousands of jobs

Brent Donnelly - Mid-April Tax Related Selling

Theme 6 - ECB ready to cut

Holding pattern until they can cut in June. As we mentioned in our previews, it was extremely unlikely that the ECB would cut but at the same time there was limited risk of a hawkish surprise as the markets and boards softer growth and inflation expectations are aligned for a June cut. Nothing to move the needle with US fixed income dominating global proceedings.

Growth on this side of the Atlantic is anaemic compared to the fiscal / AI dominance of the US. Germany is in recession, inflation is gapping lower in France, commercial real estate in Dublin is being marked down by 40/50%, China is eating into German car market etc etc... The mix of slower growth and inflation regime will allow the ECB to cut in Q2, if not sooner..

Econostream - ECB’s Lagarde: If Disinflation Progresses, the Monetary Policy Stance Will Change

Rabobank - Hinting at a cut

BMO - ECB Hold 'Em

FT - Big investors buy European bonds over US Treasuries as economies diverge

WSJ - Germany Passed its First Chinese Test---This One Is Trickier

Saxo Bank - The investment case for European equities

Theme 7 - AI dominates the headlines

The future is AI, but is it as new as many advertise? In his annual letter to shareholders, Jamie Dimon said they "have been actively using predictive AI and ML for years — and now have over 400 use cases in production in areas such as marketing, fraud and risk — and they are increasingly driving real business value across our businesses and functions."

Everyone can see the power of AI but like all new technologies it could be years before we see the real benefit. In the short term this maybe a bubble in assets but like the .com bubble/start of the internet it could be the second wave of companies/products that take over to rule. Sit back and watch this space...

JPM - Jamie Dimon's Letter to Shareholders, Annual Report 2023

Bloomberg - Trudeau Unveils $1.8 Billion Package for Canada’s AI Sector

Bloomberg - TSMC Gets $11.6 Billion in US Grants, Loans for Chip Plants

Bloomberg - Will AI Create More Fake News Than It Exposes?

Bloomberg - The Internet Cheapened News. AI Will Do the Opposite.

Nikkei Asia - TSMC expands U.S. investment to $65bn after securing $6.6bn grant

Fortune - JPMorgan CEO Jamie Dimon compares AI’s potential impact to electricity and the steam engine

Axios - JP Morgan Chase, Morgan Stanley and other big banks race to get AI right

WSJ - Energy-Guzzling AI Is Also the Future of Energy Savings

ING - AI productivity gains may be smaller than you’re expecting

Nikkei Asia - TSMC's Q1 revenue rise beats market expectations on AI boom

FT - Taiwan’s chip industry heads overseas amid supply chain shift

Macro Hive - 3 Ways AI Is Revolutionizing Finance

JPM - The Good, the Bad and the Ugly: An investor lens on tech valuations, AI, energy and the US Presidential Election.

Theme 8 - On the campaign trail

Tori-graph has been chasing Rayner, as Starmer's number 2 comes under intense pressure about her CGT bills and residency on the electorate roll. Trump is struggling to define his stance on abortion, alienating a key supporter base from '16, inflation is hurting Biden, Rishi is lining up his next job, Modi's re-election commences whilst Reform seems to be the only party that had good news last week as their support base grows at the expense of Rishi.

FT - Police investigating Angela Rayner over council house sale

FT - Inflation report complicates Biden’s campaign messaging

Bloomberg - Robust Indian Economy Fuels Modi’s Electoral Juggernaut

FT - Tory election hopes fade with prospects for interest rate cuts

FT - How Rishi Sunak built a close relationship with Blackstone’s bosses

WSJ - What Arizona's Abortion Ban Means for the 2024 Election

FT - Why isn’t Joe Biden getting credit for America’s sturdy jobs market?

Telegraph - Politics latest news: Reform UK hits highest ever level of support in new poll

WSJ - Biden’s Student-Loan Plan Seeks to Slash Debt for 30 Million Americans

Bloomberg - Trump Says States Should Set Abortion Limits, Notes Exceptions

Theme 9 - China

A quiet week from China as the focus firmly sits on the US fixed income market. We did see some negative property company headlines that the market firmly ignores. Finally, we got softer inflation in China with YoY rate printing 0.1% and below the previous 0.7% as well as the expected 0.4%. MoM was down 1% vs exp -0.5% and prior +1%.

Bloomberg - China Consumer Price Gains Fade With Industry Stuck in Deflation

SCMP - China’s low inflation set to be ‘long-term phenomenon’: 4 takeaways from March’s data

Fitch - Revises Outlook on China to Negative; Affirms at 'A+

Nikkei Asia -China Construction Bank seeks wind-up of property developer Shimao

Bloomberg - Yellen, China’s He Agree to Talks Aimed at ‘Balanced Growth’

Top 10 Reads of the Week on Harkster.com:

The New Yorker - What Phones Are Doing to Reading

Steno Research - The Bitcoin ETFs Run the World

Compounding Quality - Mastercard

BoE - Forecasting for monetary policy making and communication at the Bank of England: a review

Morningstar - Equity Strategy Monthly: Three Themes for Q2

FT - The electric vehicle revolution is running out of steam

Westpac - RBNZ April 2024 Monetary Policy Review

Man Institute - Views from the Floor - Upcoming Bitcoin Halving: A Reason to be Bullish?

The majority of these links appear in our new "HarksterPro - Intraday Market Colour" channel. If you click on "Select Channels", you should find under "Added Recently" our latest additions to the app. @HarksterHQ will use this new channel to flag good articles/sources of content as well as headlines/market moving events.

Top 5 Podcasts of the Week:

NatWest - Bucks' fizz

Macro Voices - Justin Huhn: Accelerated Demand Growth in Supply Driven Bull Market

The Inflation Guy - This Month's CPI Report - A Potential Pony Situation

The Rest is Politics - What Britain really thinks of politics

The Week Ahead

Looking forward to next week...

ABN Amro - The week ahead - 15-19 April 2024

ING - Asia week ahead: China data deluge and Japan’s inflation report

Nomura - High for Longer?

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.