The Saturday Hark Back - 10 Feb 2024

Capturing the themes of the week when there’s more time to digest them.

The Hark Back

The key narratives that drove markets last week:

Theme 1 - China Deploys the National Squad

Theme 2 - Biden vs Ackman's Twitter Account

Theme 3 - CRE vs Housing

Theme 4 - CB Speak

Theme 5 - 5000

Theme 6 - Crypto Inflow Story

Top 10 Reads of the Week on Harkster.com

Top 5 Podcasts of the Week

Week Ahead Previews

Theme 1 - China Deploys the National Squad

Chinese assets rallied into the Lunar NY, as expectations of a material shift in regulatory policy and a more "forceful" Xi intervention accelerated a short squeeze off multi year lows. These headlines/moves have occurred in the past, but the investment trend has not changed. The market wants to see something more material than just financial re-engineering. An economic turnaround is needed not just financial mechanics. With the early short squeeze now complete, Xi and his team have to deliver a large fiscal push, recapitalise the banks and much more.

In an otherwise quiet week, our dedicated China channel on Harkster.com was a focal point.

After the RRR cut, short sale ban Xi's made some more moves...

Bloomberg - Xi to Discuss China Stocks With Regulators as Rescue Bets Build

SCMP - China must shield the rest of its economy from the property contagion

Bloomberg - China Stocks Rebound as Beijing Intensifies Efforts to Stem Rout

Bloomberg - China Replaces Top Markets Regulator as Xi Tries to End Rout

Yahoo - China Share Buybacks Hit Three-Year High Amid Market Slump

China a focal point of the EV trade battle and the US election ...

WSJ - China Offers Support to Accelerate EV Makers’ Global Push

Noah Smith - Tariffs are coming

Bloomberg - Trump Floats Chinese Goods Tariff Exceeding 60% If Elected

... analysis from the west on China's outlook...

Gordian Knot - Chinese Equity Markets: Wild Ride, But "Xi Briefing" Steals the Show

Bloomberg - Wall Street Snubs China for India in a Historic Markets Shift

Reuters - Why China's national team won't save spiralling markets

Bloomberg - Traders Boost Bearish China Options Bets Even as Stocks Surged

Apollo Academy - Outlook for China: Slowing exports, housing deflating and demographics deteriorating

Gordian Knot - China Trends: Pause or Continuation? Navigating Rates, FX, and Equities

Theme 2 - Biden vs Ackman's Twitter Account

It's interesting that Bill Ackman's twitter account is no longer focused on plagiarism in academia and is instead fully focused on Biden's cognitive capabilities.

The Dems have spent the end of the week on defence after the special counsel report (Axios - Harris says special counsel report on Biden was "politically motivated"). Who would run for the Dems if it's not Biden? VP Harris? Cali Gov Newsom? Dean Philips? Marianne Williamson? Would Kennedy Jr comeback?

Despite running an economic juggernaut, Biden was already struggling in the polls behind Trump, are donors/voters simply turned off by re-electing an 81yr old president? Bill's money is already on Dean (Billionaire Bill Ackman Backs Dean Phillips to Challenge Biden).

Bloomberg reports that half of American's are miserable despite the US economy and AI equity boom driving US exceptionalism over Europe and China. How can Biden use this economic success story to encourage swing voters / undecided?

Source: Bloomberg - Good Times, Bad Times, the Fed’s Not in a Hurry

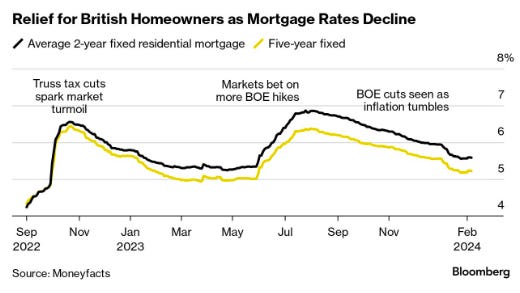

Theme 3 - CRE vs Housing

As housing recovers on both sides of the Atlantic (S&P Global - Halifax House Price Index), it's the office space that's under considerable pressure as the maturity wall approaches and workers fail to return to the office. Destination / modern offices are still performing (Adam even wants WeWork back), but any space that needs to be materially renovated / modernized is being marked down (FT - Canary Wharf office takes 60% hit in distressed sale). Furthermore, the impact of Chinese portfolio sales has increased the supply of western properties as firms look to repatriate foreign capital to shore up struggling domestic portfolios (Bloomberg - China’s Property Crisis Is Starting to Ripple Across the World). Finally, the deterioration in the German housing market is another worry for the ECB (Bloomberg - German Residential Property Dropped Sharpest on Record in 2023)

Source Moneyfacts via Bloomberg

Bloomberg - NYCB Extends $4.5 Billion Stock Rout to Lowest Level Since 1997

Bloomberg - US Commercial Real Estate Contagion Is Now Moving to Europe

Home Economics - The Office Real Estate Apocalypse is Just Beginnin

Blind Squirrel Macro - Just waitin' for the maturity wall

Bloomberg - NYCB Extends $4.5 Billion Stock Rout to Lowest Level Since 1997

Apollo Academy - Outlook for US regional Banks

Theme 4 - CB Speak

What started with Powell's Sunday night 60minute interview, was repeated throughout the week. It's too early to declare victory on inflation, more evidence is needed, the next move is more than likely a cut but we remain data dependent. The list of speakers was long and varied Mester, Kashkari, Schnabel, Breedon, Wunsch, Lane, Bullock and more ... global central banks have rolled in unison from team transitory to team higher for longer to now entering a new regime, as they remain open to cuts IF confidence rises, #team too early to declare victory.....

FT - Jay Powell says Fed expects to make three rate cuts this year

Reuters - Fed's Mester open to rate cuts if it's clear inflation is easing further

Bloomberg - Fed’s Kashkari Says Need to See More Progress on Inflation

Econostream - ECB Insight: Schnabel Pushes Back Against Market Pricing, but Carefully, Slamming No Doors

FT - Isabel Schnabel: ‘The last mile of disinflation may be the most difficult one’

Bloomberg - BOE’s Breeden Signals She’s Likely to Wait Before Cutting Rates

WSJ - RBA Keeping Options Open Regarding Further Rate Increases, Bullock Says

Econostream - ECB’s Wunsch: ‘At Some Point, We Are Going to Have to Bet on Where Inflation’s Going’

Bloomberg - Fed Has Time to Be Patient on Cutting Interest Rates, Barkin Says

BoE - Mind the gap(s): Inflation data and prospects - speech by Catherine L. Mann

Ironically the biggest rates move was from ANZ Economist Zollner... who managed to aggressively reprice the front-end of the NZ curve. 2yr rates rallied to 5% and now offer 120bps more than their antipodean cousins after Zollner called for 2 hikes when the market was eyeing the next move as a cut.

As Brent Donnelly highlights, "RBNZ governor Orr is set to speak Thursday afternoon. That should be a huge event given the overnight moves and the fact that the February meeting is priced close to 50/50." (Zollner is the new Evans) ... will Orr endorse or pushback against Zollner's call.

Finally, BoJ Gov Ueda echoed Deputy Uchida's comments.... the message is clear, they will leave negative territory but rates will stay very low thereafter

Bloomberg - BOJ’s Uchida Says Hard to See Sharp Hiking Pace Post-Liftoff

Brent Donnelly - A Great Speech

Theme 5 - 5000

Another week, another set of all-time highs. Lower vix, lower cross asset vol, momentum, strong equity earnings season, strong US growth, soft landing vibes, strong real wages, isolated fears (recession risk, CRE portfolios etc), Trump leading in the polls supporting Business leaders' optimism and AI productivity boom. The Mag 7 cash machine keeps driving performance, the S&P 500 excluding tech is trading at all-time lows against tech stocks in the index...

Source Bloomberg via @BarChart

MacroHive - Equity View: What Is Booming in the AI Ecosystem (and What Is Not…)

WSJ - UBS Can Be the Next Morgan Stanley, but a Lot of Things Have to Go Right

FT - Uber posts first full-year operating profit and boosts buyback hopes

Compounding Quality - Simple Path To Wealth, Buying a new ETF

Theme 6 - Crypto Inflow Story

As the halving approaches, VIX slides and US fixed income vol subsides, Bitcoin is rejoicing a positive etf inflow story as it returns to 47k and its 2024 highs. According to ZeroHedge, "Yesterday saw the third largest net inflow into spot Bitcoin ETFs, totaling over $400 million with iShares Bitcoin Trust (IBIT) seeing over $200 million inflows alone, dominating the $101 million outflow from GBTC..."

ZeroHedge - Bitcoin Soars To Post-ETF-Launch Highs As Net Inflows Explode

Ecoinometrics - Bitcoin ETFs: winners and losers

Coingraph News - “Identity of Bitcoin Creator Nakamoto Sparks Rumors”

Top 10 Reads of the Week on Harkster.com:

M&G Investments - The Traitors – can a game of human psychology draw parallels with bond markets?

MS - Key Themes for 2024

Bloomberg - Elon's Cage Fight With Zuckerberg Just Happened. He Lost

Stenos Signals - Breaking SLOOS survey: The US economy is accelerating and inflation risks are back!

Man Group - Are Markets too Complacent on Inflation?

The Lead-Lag Report - Credit Card Delinquencies Surge 50%

Steno Research - Inflation Watch: Adjusting for revisions, tax, seasonality and sunspots

FT - Blinken pushes for ‘enduring’ Gaza peace deal in Riyadh visit

FT - Me, Taylor Swift and the Super Bowl plot to save America

FT - Who are the candidates vying to be Trump’s running mate?

The majority of these links appear in our new "HarksterPro - Intraday Market Colour" channel. If you click on "Select Channels", you should find under "Added Recently" our latest additions to the app. @HarksterHQ will use this new channel to flag good articles/sources of content as well as headlines/market moving events.

Top 5 Podcasts of the Week:

DB CIO Weekly - More jobs, no early cuts

MS Thoughts on the Market - Which Geopolitical Events Matter Most to Investors

JPM Global Data Pod Research Rap - US core inflation to bolster Fed confidence

Barry Ritholtz - MiB: David Einhorn, Greenlight Capital

BlackRock - GenAI Through A COO Lens

The Week Ahead

Looking forward to next week...

After Monday looks set to be quiet, due to the unofficial long weekend in America following Taylor Swifts first appearance at a super bowl, Tuesday's US CPI print will dominate proceedings...

ABN Amro - The week ahead - 12-16 February 2024

Nomura - The Week Ahead – US CPI and Retail Sales, UK CPI and Labour Market Data

SEB - All eyes on US CPI

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.