The Morning Hark - 25 Oct 2023

Today’s focus...PMIs this side of the Atlantic do little to lift the gloom, Beijing tries to lift their gloom as Xi pops in for a cup of tea, the RBA looks to be in play again and a BoC sleeper.

Overnight Highlights

Prices are at 7.00 BST/2.00 EST, with changes reflecting movement from midnight BST

Oil - Brent and Crude December futures off a touch in Asia with them currently at 87.70 and 83.40 respectively. Tough day for the oil bulls yesterday with the poor PMIs, especially out of Europe and the UK, adding to demand worries. The fall in oil came even with the API data showing that US crude stockpiles had fallen last week.

EQ - Asian equity markets buoyed by the economic stimulus announcements from the authorities in China with the Hang Seng up over one percent to 17,185. The Nikkei also bid at 31,250.

The US indicies off a touch in Asia with the Nasdaq and S&P futures at 14,780 and 4258 respectively.

Gold - Gold Dec flatlining in Asia once again with it currently sitting at 1983.

FI - Global yields steady overnight with the US2y and US10y trading flat at 5.06% and 4.83% respectively. Calmer day yesterday after Monday’s fireworks as the market bides its time for the next directional move.

European yields pushed lower after the poor PMIs with the German 10y yield closing the day at 2.83% and the Italian 10y yield at 4.84%.

UK gilt yields similarly so at 4.54%.

FX - Really quiet in FX overnight with the USD Index currently flat at 106.20. The JPY, EUR and GBP similarly flat currently at 149.85, 1.06 and 1.2170 respectively.

The USD recovered some of the high ground yesterday after the contrasting PMIs emphasised the different stages that the major European economies are in comparison to the US. As we said yesterday the EUR looked over extended and we felt that the PMIs would be the catalyst for a retracement. If the PMIs are to be believed, and indeed Lagarde alluded to it with her comments yesterday, Europe is in for a tough few quarters. In contrast the US has started the fourth quarter as it finished the last one with resilient economic prints. The Fed have warned that this quarter should see a slowing in the data. Let’s see what it brings but on first look you’d rather be long USDs.

The AUD had a decent rally post inflation print capturing 0.64 for a two week high. Currently at 0.6380

USDILS continues with the bid tone at 4.0640.

FX expiries of note today in the AUD we have AUD1.6bn at 0.6300 which post the inflation print seems a bit away. GBP sees about £2bn layered between 1.2100/40 and the EUR has €1bn at 1.06 and 1.0540.

Others - Bitcoin and Ethereum holding onto the majority of their gains from yesterday with the pair currently at 34,020 and 1785 respectively.

Macro Themes At Play

Recap

Germany hardly set the world alight with its flash PMIs. Manufacturing scrapped over the 40 mark to 40.7 beating both last months and expectations. Services meanwhile slumped back into contraction at 48 with downside misses on both previous and expectations. Stuttering at best.

Far from enamouring quotes either; “Continued downward pressure on demand for goods and services”, overall inflows of new business posting the steepest decline since May 20” and service firms reported their worst sales performance for almost three and a half years.

The EU followed in Germany’s footsteps with downside misses across the board. Manufacturing clocking in at 43 and services 47.8, the low for the year, in what was described as an ever weakening demand environment and a near 3 year low for the private sector’s performance.

Meanwhile in the UK some very small crumbs of comfort with manufacturing beating the previous month’s print and consensus at a rip-roaring 45.2 whilst services came in a smidge lower than expected and previous at 49.2.

God bless America! They rescue the day with upside beats for both the US manufacturing and services PMIs at 50 and 50.9 respectively.

Overall the PMIs illustrate the gulf between Europe and the US. The BoE and ECB are a lot closer to a policy shift than the US are which should help support US yields and the USD. This side of the Atlantic it feels like a race to the bottom.

Meanwhile reports suggest that the BoJ is mulling whether to tweak their YCC over US yield concerns or perhaps just do some more “unscheduled” bond purchases?

Overnight

The major news overnight was the economic stimulus packages announced in China to boost the economy. The authorities issued a further $140bn of sovereign bonds in addition to raising the budget deficit ratio from March’s 3% of GDP to above 3.8%. Xi even popped into the PBOC for a cup of tea and a chat to rally the troops.

Hong Kong also introduced measures to help stimulate their economy.

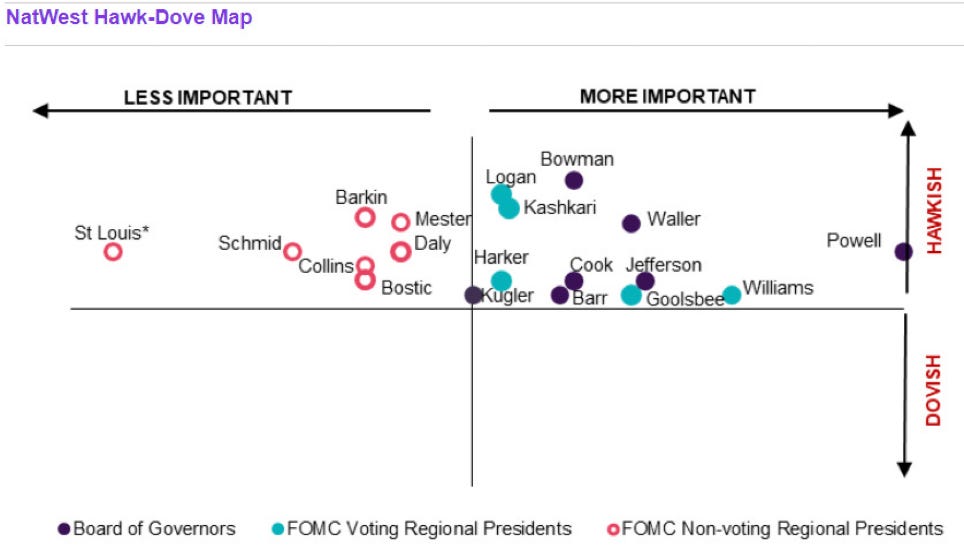

For those that missed it yesterday I thought I’d post this very useful chart from NatWest again regarding the make up of the FOMC…..pictures/a thousand words and all that.

Central Bank Speakers

ECB’s Lagarde was reported to mention in her message with EU officials that the fight with inflation was going well but that the EU zone would stagnate for the next few quarters.

RBA’s Bullock noted that the RBA is mindful of policy lags and that consumption and inflation have slowed. She also referenced the fact that the RBA would get more information before its November meeting including updated forecasts. More importantly, given the inflation report, she stated that the RBA would not hesitate to raise rates if there is a material upward revision to the inflation outlook.

The Day Ahead

The Australian inflation report for q3 makes the RBA meeting on 7 November very much a live one. All measures came in a tick higher than expected with QoQ at 1.2% and annualised at 5.4%. This following on from Governor Bullock’s hawkish comments yesterday it seems that a further hike from the RBA is a distinct possibility. We get both Kent and Bullock speaking late this evening so keep a look out for further signals from them.

Westpac - Aussie Inflation Report

German Ifo following on from yesterday’s poor PMIs doesn’t bode well.

Not so knife edge BoC rate decision, policy report and subsequent press conference. Should be a sleeper.

Powell and Lagarde speak but its hard to see them adding anything new to the landscape.

👍 If you found this morning’s briefing helpful, please consider giving it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience.

Follow the latest market narratives through our curated research & commentary channels on Harkster.com

Main Highlights Ahead

All times in BST (EST+5 / CEST-1 / JST-8)

The main highlights for the day ahead in terms of data and speakers:

Wednesday

Germany Ifo Business Climate Oct consensus 85.9 vs previous 85.7 (09.00 BST)

Germany Ifo Expectations Oct consensus 83.3 vs previous 82.9 (09.00 BST)

BoC Monetary Policy Report (15.00 BST)

BoC Interest Rate Decision rates expected to remain on hold at 5% (15.00 BST)

US New Home Sales Sept consensus 0.68m vs previous 0.675m (15.00 BST)

BoC Press Conference (16.00 BST)

RBA Bullock speaks (23.00 BST)

RBA Kent speaks (23.00 BST)

Fed Speakers

Powell (21.35 BST)

ECB Speakers

Lagarde (18.00 BST)

Good luck.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

Like the Hawk/Dove Fed Chart......