Read on the Trading Floor - 31 Oct 2023

Today’s focus… BoJ and pressure on equity valuations

Macro Themes At Play

Theme 1 - BoJ reveals minor tweaks, USDJPY tests 151.00

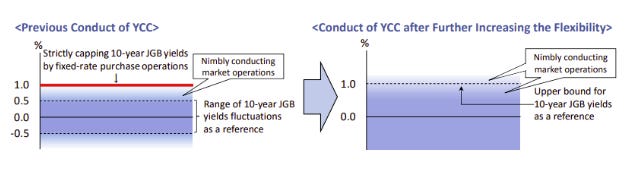

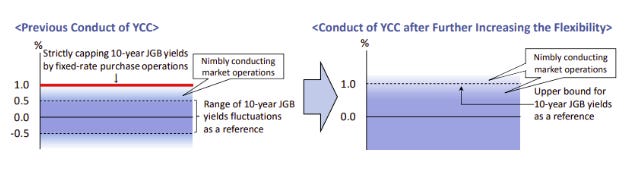

Reference rate is now a nimble target around 1%, not a rigid limit. Gone are unlimited BoJ bids at 1%, giving the market greater flexibility to set the price.

Gov Ueda declared that it is now "appropriate to increase flexibility so that long-term yields can be smoothly shaped, according to different future scenarios"

he also said "... we still haven't seen enough evidence to feel confident that trend inflation will (sustainably hit 2%)...as such, we don't see a big risk of being behind the curve"

This statement came after they raised their inflation forecasts across the board. 2023 to 2.8% (prior 2.5%), 2024 to 2.8% (prior 1.9%) and 2025 to 1.7% (prior 1.6%).

In summary, we're another step closer to the dismantling of YCC. Rather than ripping the band aid off, they're getting their slowly and surely. They've dropped unlimited interventions, abandoned their daily fixed-rate bond buying operation and bought greater flexibility around 1%. BoJ will steadily reduce their influence on the price of JGBs... crucially JPY longs are still receiving negative rates.

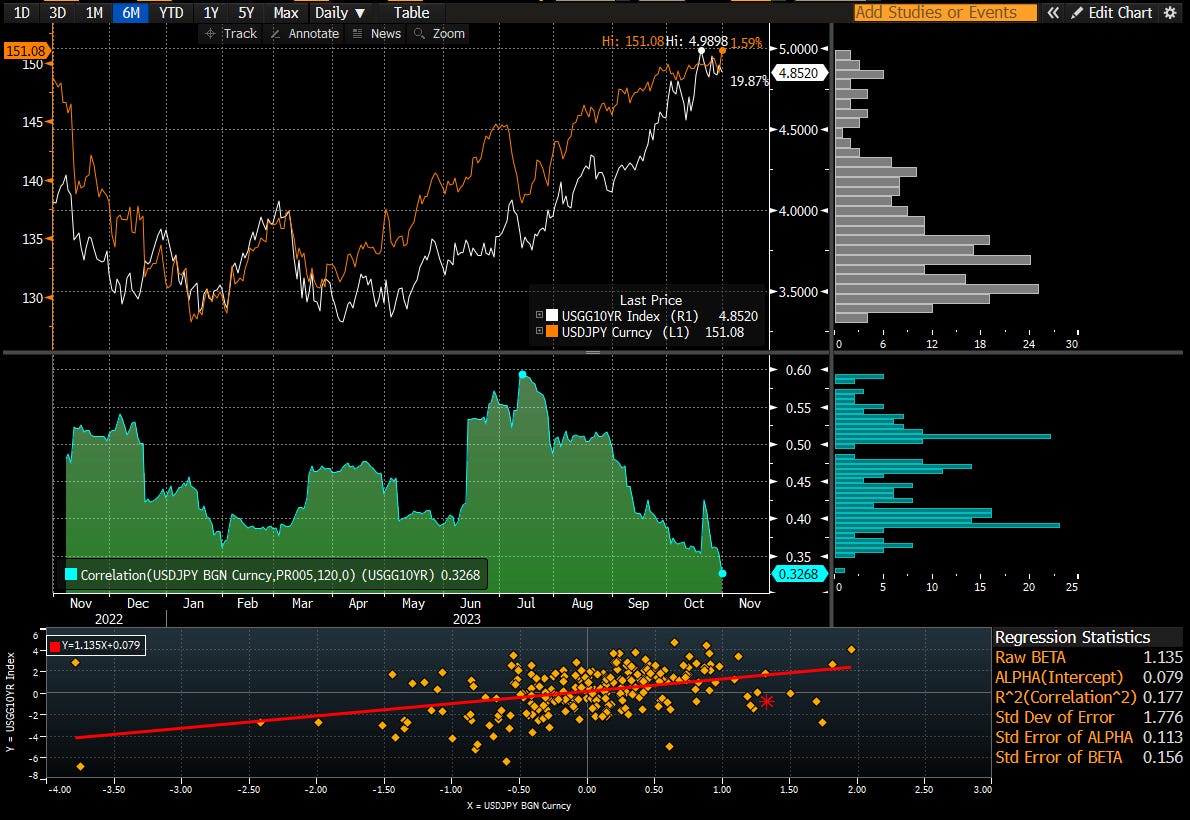

So naturally the market will test where they will appear in JGBs and of course in FX... which leaves us with the Fed and Treasury Refunding announcement as the key events this week. Today we've seen 2s, 5s, 10s trade a little lower initially, which is often the case as we may be seeing some duration rebalancing demand into month end. However, as the hotter ECI print (1.1% vs exp 1%), USDJPY has turned higher in-line with the broader DXY move as rates sell off back to their overnight wides. The true turn in USDJPY comes when a US recession generates a meaningful move back into US duration ...

Bank of Japan reviews curated from Harkster.com

ING - Bank of Japan disappoints markets again despite another YCC tweak

Brent Donnelly - Out of -GBP into -CADJPY

Steno Research - The most hawkish BoJ in decades?

USDJPY vs US 10s ... correlation has dropped since the middle of the summer

Source Bloomberg

Theme 2 - Equity correction (SPX now -10%) but it is not yet a capitulation

#1. Financing Costs on the rise in Earning Calls

Source BofA via @MikeZaccardi

#2. JPMorgan's Kolanovic Says Earnings Estimates Are Divorced From Risks

Bloomberg - Earnings Estimates Should Be Revised Lower

#3. Plenty of headlines on Twitters X's new valuation ...

@HarksterHQ is not a tax / accountant expert but is it a good time for Elon to take a large write down? Is there only upside left from here, all the bad news in the price? Does he harvest large tax write-offs from the loss?

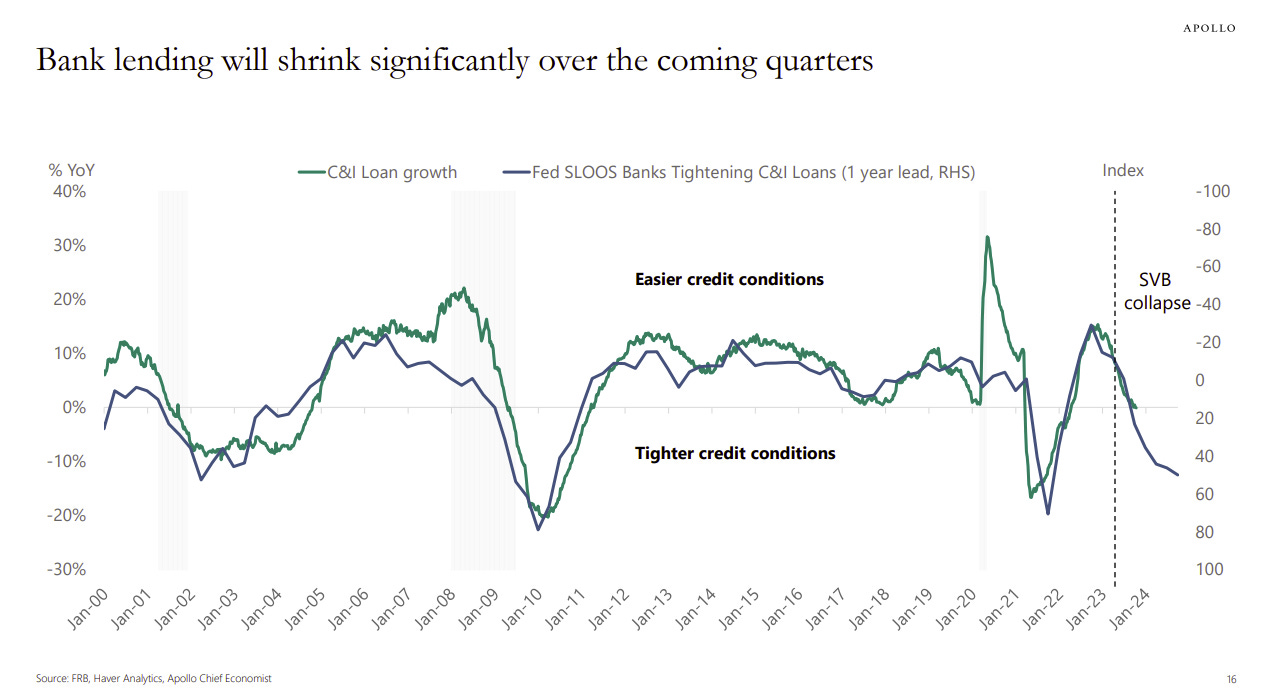

#4. Apollo - Outlook for Banks and a significantly slower US economy as lending tightens

#5. Man Institute: Views from the Floor ... The Spectre of a US shutdown: How spooked could government sensitive stocks get?

Sector concentration is highest in Industrials (35%), Healthcare (20%), and Technology (15%)

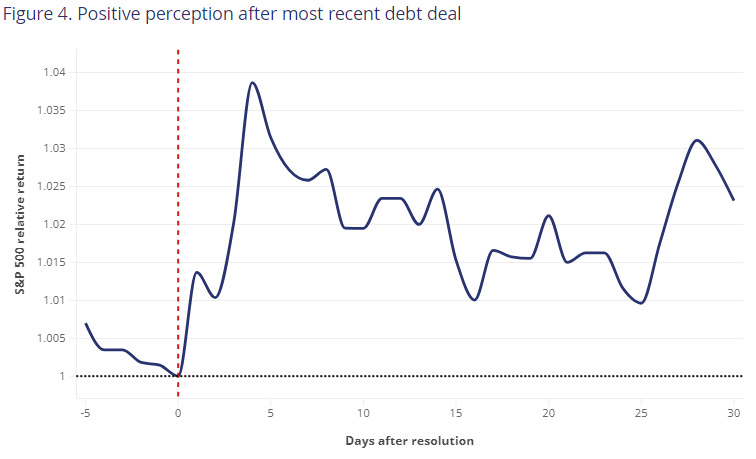

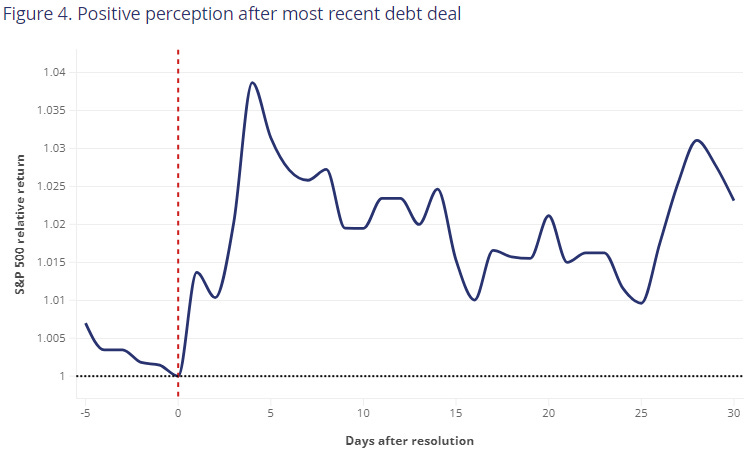

Negative perception leading up to debt limit deadlines ... positive perception after debt deal. As a result, the Man Institute “observed excess returns reaching around 1.9% over the two weeks following the bipartisan Fiscal Responsibility Act (2023) passage by both houses of the government on 1 June 2023, as shown in Figure 4.”

Source: Man Numeric

#6. Caterpillar down 5% on weak forecasts, slowing demand.... a global economic bellwether?

ZeroHedge - CAT Plunges After Order Backlog Unexpectedly Shrinks For First Time Since 2020

Reuters - Caterpillar shares fall on equipment demand concerns despite earnings beat

ㅤㅤㅤ

👍 If you found this piece helpful, please give it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience.

Top Pieces

Discovered on Harkster.com

Israel struck targets in Lebanon and Syria overnight

Apple goes after AI market with new processors as iPhone lose further ground to Huawei in China

The BondBeat - USTs bull flattening on heels of BoJ, China PMI disappoints; STRONG volumes

Bloomberg's Ven Ram via ZeroHedge - Higher Neutral-Rate Expectations Show Why Treasuries Hugging 5%

ING Rates Spark - UST brave the first supply test

Eurozone Inflation and Growth

ㅤㅤㅤ

Stay informed throughout the day with our new commentary feed (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

ㅤㅤㅤ

ㅤㅤㅤ

ㅤㅤㅤ

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.