Read on the Trading Floor - 30 May 2024

Today’s focus… yields: supply, data and month end

Macro Themes At Play

Theme 1 - South Africa Coalition

Theme 2 - What starts in Japan, reverberates around the world...

Theme 3 - Buyers strike in Fixed Income?

Theme 4 - but softer US data helps cap yields

What's being read on Harkster.com

Theme 1 - South Africa Coalition

ZAR is off its weakest levels on the day, in line with the rally in US 10s. However, the backdrop of an ANC coalition is certainly disappointing for the mkt. How can the ANC deliver on fiscal savings without strong coalition supporters? Will they turn to Zuma's MK party for support? As Emerging Market Watch have indicated, an ANC party in the low 40s "would not be able to rely on smaller centrist parties alone to help it pass key money and other bills which require an absolute majority."

Emerging Market Watch - South Africa: ANC stands to gain 43.2% support with 20% of votes counted

Reuters - South African election early results see ANC losing majority, DA and MK performing well

Oxford Economics - South Africa: Elections 2024 | Counting underway after calm voting day

Source: Tradingeconomics.com

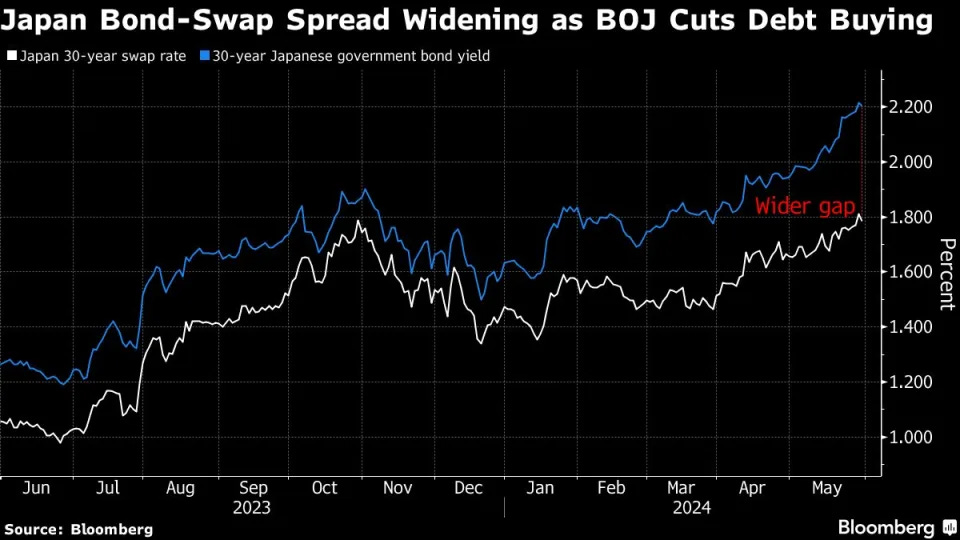

Theme 2 - What starts in Japan, reverberates around the world...

As Japanese 10yr yields drift wider, breaking ~1.00% that was once defended by the BoJ with unlimited buying, expectations are growing that the BoJ will reduce their QE program at the June meeting. This can also be seen in the 30yr trend that sees the bond/swap rate widening to the most since 2012. (Source BNYM - Japan’s 30-Year Bond-Swap Rate Gap Widens to Most Since 2012)

The higher the yield Japanese investors receive at home, the more they ask from global governments to compensate / attract their savings. The BoJ YCC dampener has been removed from global FI markets...

Source: Bloomberg via BNYM

Theme 3 - Buyers strike in Fixed Income?

Disappointing 2/5/7 auctions this week as the market struggles to ingest the historic issuance. Hedgopia.com posted the chart below, flagging the $1trillion in interest payments from Treasury. That’s a lot of money entering savings accounts, pension funds and of course corp balance sheets (apple...????) ... How can the Fed mop it up?

Bostic once again confirmed a Q4 move as the earliest, he is still believes there is a way to go as the breath of inflation is still quite high. Logan and Williams are next on the Fed docket.

ING - Supply indigestion

Fidenza Macro - What's behind the jump in global yields?

Bloomberg's John Authers - Throwing in the Towel on Rate Cuts Everywhere

Hedgopia.com - On Back Of Soft Demand For Treasury Auction, 10-Year T-Yield Rallies To Upper End Of Symmetrical Triangle

Bloomberg - Fed’s Bostic Says Many Inflation Measures Moving to Target Range

Theme 4 - but softer US data helps cap yields

Looking in the rear-view mirror, the second Q1 GDP print is now 1.3%, down 0.3% from the advanced 1.6% reading as consumer spending was revised downward, consumption slowed more than first thought. Initial claims also drifted higher, 219k is close to an 8month high and as a result, US10s drifting off 2-week wides, rallying down to 4.57% off 4.62%.

However, this data is all just a prelude to what we've been waiting for all week, "the Fed's favourite inflation indicator" will be released tomorrow afternoon, 0.3% Mom doesn't get us to 2% target.

Despite the buyer's strike, month end is normally a good period for duration. BofA via The Bond Beat highlight "with the S&P total return in the month to date at c.5.5%, the 10-year+ UST index c.3.5% total return over the same period, and corporates c.1.8%, the expectation is for rebalancing flows out of equities and into fixed income for the month (with corporates favored over USTs in the rebalance)."

Advisor Perspectives - Q1 GDP Second Estimate: Real GDP at 1.3%, Below Forecast

Calculated Risk - Weekly Initial Unemployment Claims Increase to 219,000

The Bond Beat - while WE slept: May 30

What's being read on Harkster.com

Gold is cheap?, Red Bull Leeds, 22 of 29 economists expect BoC to cut, US focuses on Russia's supply chain as Ukraine losses ground, can you turn off Meta AI and finally, as orange/food prices squeeze commodities are in focus this summer.

Metals, oil and everything else - gold is cheap

The Telegraph - Red Bull buys stake in Leeds to enter English football for first time

Bloomberg - Traders Are Bracing for a Record-Smashing Summer That Will Shake Up Commodities

Compounding Quality - Set it and forget it

FT - US seeks to choke off supplies via China for Russia’s war machine

FT - Germany to scrap gas levy over neighbours’ threats to boost Russian imports

Reuters - POLL BoC to cut interest rates on June 5, three further times this year

The Telegraph - Putin’s plot to destroy Nato is reaching its devastating climax

Stay informed throughout the day with our new commentary channel (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.