Read on the Trading Floor - 14 Dec 2023

Today’s focus… Powell pivots as Lagarde/Bailey pushback

Macro Themes At Play

Theme 1 - and you thought JPow wouldn't be able to stick the soft landing

Theme 2 - If the Fed is easing, where do you want to invest your money?

Theme 3 - Hawkish CB's in Europe...

Theme 4 - Will 10 years stick sub 4%?

Further reading and listening of note

Theme 1 - and you thought JPow wouldn't be able to stick the soft landing

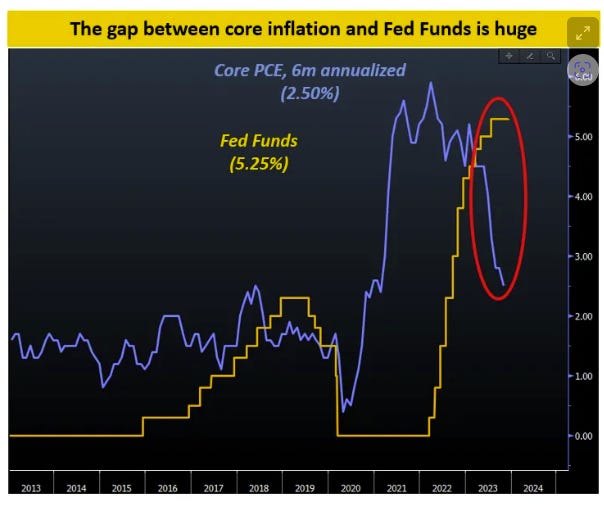

It is most certainly the season of good will and cheer, and boy did JPow deliver. The arch dove showed his true colours, setting the world a blaze with cuts and comments...

Policy "well into restrictive territory"

"Very focused on not making the mistake of keeping rates too high for too long"

They will need to cut well before 2% target is reached

“Cuts are beginning to come into view and are now a topic of discussion”

The Macro Compass believes the Fed doesn’t want real Fed Funds at 3%+ (too restrictive) but at 1-1.5% (mildly tight).

Source: The Macro Compass - The Pivot Is Here

As a result today has been a race for strategists to mark to market their rate cut expectations (Bloomberg - Goldman Sachs Revises Fed Call, Now Seeing ‘Earlier and Faster’ Cuts).

In terms of short-term positioning, Powell has hurt a few participants, delivered a few bags of coal to those on his naughty list who had the audacity to think he might be hawkish!!!! Some entered the event paid front end US rates, looking for a September repeat... H4L and pushback against the excessive easing priced into the curve. I guess the way BoE and ECB behaved despite substantially weaker backdrops.

Furthermore, the market is not positioned for this move in EURUSD. At 1.08 the Q1 focus was lower, as the diverging growth, inflation and fiscal dynamics on opposite sides of the Atlantic led to premium being spent on sub 1.05 strikes for the end of Q1. Afterall, if the US needs 75bps, Europe will need more and sooner but Lagarde failed to match let alone beat JPow's dovishness. EURUSD is sometimes the worst way to play European growth dynamics, as it sits in the middle of the ACB recycling basket and the single ccy is forever the anti-USD before it is a play on European growth.

Theme 2 - If the Fed is easing, where do you want to invest your money?

Pre-meeting

highlighted their study which shows the 90.90% likelihood of a new high printing after unwinding the recent bear market decline... (Nautilus Research - The "Magnetic" Attraction of Prior All Time Highs)The Gryning Times - (No More Resistance?) highlights the Russell 2000 is 26% away from the all-time highs marked two years ago.

"there's one major data point for markets between now and year end, and it's the Fed's favored inflation gauge, core PCE. But now we don't have to wait for it. Powell leaked it yesterday afternoon, in his press conference prepared remarks - they expect it to have fallen from 3.5% to 3.1% year-over-year."

Is there a better place than Brazil? The home of football will be hosting an NFL international game next year and relative to its Mexican cousins has underperformed in 2023.

is building a Brazilian basket (Samba Time!)Elsewhere the "everything rally" trade ideas continue to perform, including unprofitable tech stocks, regional US banks and battered Swedish real estate.

(Fed dovishness is appreciated by the market) warns valuations and technicals suggest some sectors are vulnerable to a pullback in the short-term.Finally,

has headed to commodities (The Most Important Chart for 2024) as does SAXO Bank (Fed’s dovish tilt adds fresh fuel to precious metals)Theme 3 - Hawkish CB's in Europe...

ECB - risks to economic growth tilted to the downside, PEPP brought forward to the second half of the year so cuts and QT are not overlapping and a clear push back on excessive market pricing. EURUSD hits 1.10 as the spread between Italian / German bonds dropped below 170bps as some investors feared a sudden or March PEPP taper.

Livesquawk - ECB Keeps Rates Steady, Warns of Near-Term Inflation Bump

Bloomberg - ECB Holds Rates With Inflation Sinking But Hastens Bond Exit

Econostream Media - ECB’s Lagarde: Work Still to Be Done, but This Can Take the Form of Holding Rates Steady

Nordea - ECB Watch: Tunnel Vision

Norges - In the face of softening data, weak oil prices and a slower Europe, Norges still delivered a hike and would like a stronger NOK

BoE - Too soon to pivot as core inflation lags US and Europe whilst wages are growing faster.

ING - Bank of England pushes back on calls for early 2024 rate cuts

The NY Times - Europe’s Central Banks Are Not Ready to Even Talk About Cutting Rates

FT - Stubborn inflation prompts Bank of England to diverge from the Fed

Theme 4 - Will 10 years stick sub 4%?

We're entering a period, when seasonals point to higher yields. The last few weeks of a year, ahead of a wave of Q1 issuance can put pressure on rates markets as portfolios make room for new paper. Furthermore, if the Fed has gone too early when those with softer growth dynamics are pushing back, could we see a steeper curve as the mkt fears inflation being re-ignited? Finally, January will also bring Yellen's next funding announcement for the treasury.

Brent Donnelly - "If the Fed has pivoted a bit too early and inflationary pressures return, it’s not bullish bonds." (am/FX - Logical Outcomes!)

- - Bull Steepening Watch - Is lower yields really what risk assets?

Capital Flows and Asset Markets by

- HAS INFLATION BEEN CONQUERED?

ㅤㅤㅤ

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

Top Pieces

Discovered on Harkster.com

Fortune - JPMorgan says ETF optimism is overhyped, and Ether could overshadow Bitcoin in 2024

- - SPX RETEST DAILY 3

UBS CIO Global Livestream - New Year’s Portfolio Resolutions

Stay informed throughout the day with our new commentary channel (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.