Read on the Trading Floor - 13 Feb 2024

Today’s focus… Fed expectations repricing, XBT inflows, Ceasefire in the middle east and much more

Macro Themes At Play

Theme 1 - It was too early to declare victory on inflation

Theme 2 - Both sides of the Fed mandate are running stronger than expected

Theme 3 - Swiss inflation supports the markets bearish CHF view

Theme 4 - XBT hits a two-year high

Theme 5 - De-escalation in the Middle East?

Further reading and listening of note

Theme 1 - It was too early to declare victory on inflation

March is dead in the water and now the market has been forced to push the first cut from May back into June. Narrowing the spread between market pricing and the SEP dots as well as Fed rhetoric of 3 cuts this year. The inflation trend is softer, it's just not as soft as expected. The market called for 2.9% and has instead been hit with a 3.1% YoY which is softer than the prior 3.4% but just not soft enough for those betting on a March or even a May cut. If headline disappointed, core was worse as it remained at 3.9%. The MoM reading of core also rose 0.4%, the fastest monthly rise since last May.

Inflation is being driven by a re-acceleration of core services... hotel stays, airfares, medical care, owners equivalent, health insurance and transport services all kept the MoM supported (UBS CIO First Take - January CPI print with Brian Rose). Without the substantial deflation in second hand cars, apparel and other core goods sectors this would have been a truly shocking print for the market and the data dependent Fed.

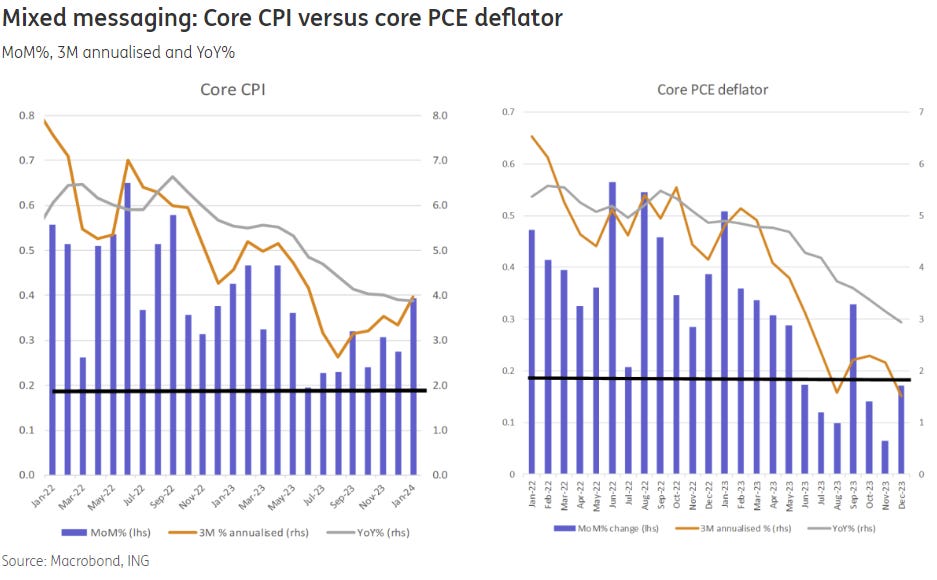

In fact, the Fed are stuck in a world with mixed messages... as core remains sticky but their PCE deflator does not. "The Fed's favoured measure of inflation, the core PCE deflator, may be cooling nicely, but the mixed messages mean the Fed can't relax, with little inclination for imminent rate cuts"... (ING - Sticky US inflation reaffirms Fed caution on rate cuts). Powell and Co are extremely lucky that the economy is not screaming out for cuts. It would be much harder to buy time if the US had hit the recession so many expected by now.

As one would expect US fixed income market have repriced as the 3month trend in US2s is now well and truly broken. The US economy just isn't ready for cuts as much as the financial world wants them. 10s is up 11bps to 4.28% whilst 2s also sold off +13bps to north of 4.6% as the Fed. There will be cuts just not this side of Easter.

Source: Tradingeconomics.com

Calculated Risk - YoY Measures of Inflation: Services, Goods and Shelter

WSJ - Inflation Tracker: At 3.1%, See the Items Keeping Prices High

Steno Research - USD inflation review: Powell has to invent a new measure..

UniCredit - US CPI: A disappointing January report

Theme 2 - Both sides of the Fed mandate are running stronger than expected

The committee's confidence in the incoming data bringing inflation back to target will be dented. In fact, questions will now be asked if we're in danger of entering a "sticky" inflation regime as we commence down the "last mile" of the fight against inflation. Real wage gains, potential election year give aways, energy prices rising, housing market stabilising, strong consumer spending in Nov and Dec and of course the bumper NFP as the solid jobs market remains at historically strong levels .... The economy is cooling, still making progress towards their 2% target, just not at the pace the market had expected. This is the second straight inflation print to surprise to the upside as domestic price pressures are far from tamed. There was always going to be a high bar for the Fed to cut when the US economy was chugging along at 3% growth in Q1, now inflation has closed that window.

E-piphany by Mike Ashton - Inflation Guy’s CPI Summary (Jan 2024)

Was there any good news? Super core has drifted sub 3%, back on a 2 handle which will give the Fed some glimmer of hope but with

Source: FT

Theme 3 - Swiss inflation supports markets bearish CHF view

A trade the market has liked in February has been the contrasting divergence between the inflation outlooks that the SNB and Fed are fighting. The former has seen an aggressive deceleration in price pressure today with headline now at 1.3% vs the expected 1.7%. Core was also 1.2%, well below the 1.6% forecast. Expectations will build into the March SNB quarterly meeting that the SNB will look to adjust their FX policy and no longer look for Franc appreciation.

Source: Tradingeconomics.com

Theme 4 - XBT hits a two-year high

Steady ETF inflows, cleaner positioning after the Grayscale induced supply that force a dip below 40k and of course the natural gravitational pull towards the halving... Crypto is back and the market is chasing the golden ticket to a funded retirement .... (The Pomp Letter - Can The Average Person Retire By Buying Bitcoin Today?)

The Wolf of All streets - The Wolf Den #902 - $50000

Unchained - BTC's Two Year High

The Bitcoin Layer - $100k Bitcoin Is Closer Than You Think

Theme 5 - De-escalation in the Middle East?

Biden is pushing for a 6-week ceasefire as CIA/Mossad set to meet along with Egyptian and Qatari officials. This would be a positive surprise to the global outlook as many fear a prolonged regional crisis will maintain elevated freight costs and potentially postpone G10 CB cuts.

FT - CIA and Mossad chiefs to hold talks on Hamas hostage deal

Reuters - US, Jordan throw their weight behind Gaza ceasefire effort ahead of new talks

Steno Research - Why Gaza Ceasefire is Coming Within 2 Weeks

ㅤㅤㅤ

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

Top Pieces

Discovered on Harkster.com

Man Group - Big Tech Valuations – are we partying like it's 1999 or is this just 1997?

GS Podcast - 2024: the year of elections

SpotGamma - The OPEX Effect: Feb Edition

Capital Flows and Asset Markets - CAN WE ONLY GET A BEAR MARKET WHEN THE BOJ ENDS QE?

FT - Resilient wage growth gives BoE new grounds for caution on rate cuts

Stay informed throughout the day with our new commentary channel (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.