Read on the Trading Floor - 06 Oct 2023

Today’s focus… #MAGA Jobs adjustments, valuations, week ahead previews and more

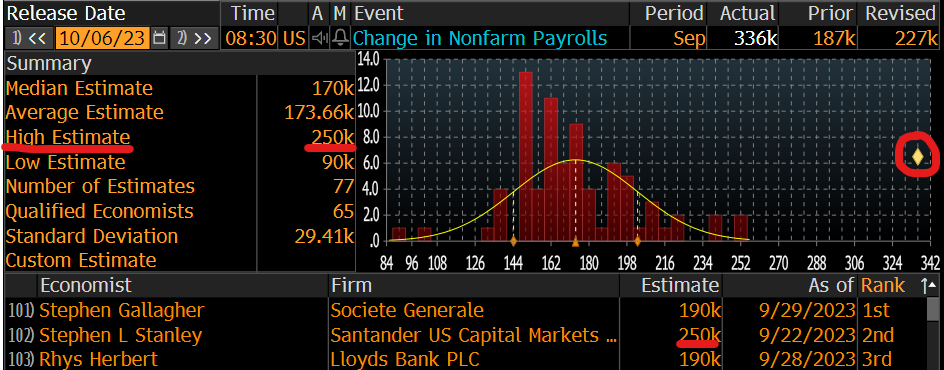

Theme 1: US Labour Market .... #MAGA adjustments?

After a week of mixed labour data from Jolts, AHE, ADP and ISM, today's NFP dominated sentiment after a historical miss. It was outside the range of the Bloomberg Economist Survey.... a 6 sigma beat (ZeroHedge). Simply mind blowing... all that computer power, all the PHD's spending weeks forecasting the number and the whole street missed the dart board, no one was even close! Like Jordan Speith trying to hit a fairway at the Ryder Cup.

Source Bloomberg

The fiscally fueled post covid US economy just won't die, no matter how many leading indicators point to stagflation or a slowing housing market, the labour market won't crack. We shouldn't be surprised as IJC sits at record lows and we need to see a 3/4 weeks of a steady trend of claims rising towards 300k before we should EVER consider the labour market is normalizing. As @darioperkins tweeted this afternoon "The US labour market can stay "pre-recessionary" longer than bond bulls can stay solvent"

But was the issue with the economist models or the BLS "seasonal adjustments" .... @VPatelFX via ZeroHedge - Inside Today's Jobs Report: 885,000 Full-Time Jobs Lost, 1.127 Million Part-Time Jobs Added, Record Multiple Jobholders.

The miss was so big and out of sync with other signs in the economy, it's not a surprise as the dust settles into the close to see the USD, bonds and equities reverse some of the initial shock. The key now is to see if this forms a blowout top for yields / USD ... next week's CPI will be key (more below).

Some further reading of note

Mish Talk - Government Jobs Rose by Nearly 1 Million Unadjusted in Sept, What Going On?

Mish Talk - Jobs Unexpectedly Surge by 336,000 But Employment Only Rises by 86,000

Axios - Why markets shouldn't sweat the blockbuster jobs report

am/FX - Closing Levels Are Key

Economic Policy Institute - Job growth is strong, wage growth continues to normalize

Theme 2: Raging Yields and its Impact on Valuations from private markets through to utilities!

As can typically be the case, it's been a quiet start to the month, amplified by the Chinese holidays. One theme that has been percolating on Harkster.com is the liquidity withdrawal from Global CB's and in particular what "Higher for Longer" + QT means for credit, equity and bond markets. After a decade of ultra-low rates, the market is worried once again about the maturity wall and its impending impact on public as well as private assets. There is now an alternative (TINAA), as the yields on 10yrs equals the dividend on SPX. After ignoring gravity through the summer, Nasdaq is finally catching down to the sell-off in rates, the focus and speculation continues around PE (self)valuations, some big-name commentators calling for 20% market plunges (h/t JPM's Kolanovic), FinTwit overlaying charts of Black Friday Sell off and yields recent rise ... even utilities are getting hit by the repricing in TLT (The Last Bear Standing - Yields Nuke Utes)

"Surety of cash flow doesn't protect overvaluation in utilities as the correlation with TLT"

Source: The Last Bear Standing

The FT have written an excellent piece Who feels the pain from the bond sell-off?

"Paper losses on the most opaque part of US banks’ bond portfolios are now close to $400bn — an all-time high, and 10 per cent above the peak at the start of the year that caused the collapse of Silicon Valley Bank — according to Matthew Anderson, an analyst at bond data firm Trepp. Most banks, and in particular the largest ones, will not have to sell and so will never realise those losses.”

Some further reading of note

The Inflation Guy / Michael Ashton - Higher Rates' Impact on Levered Strategies

Russell Clark - Finally Putting My Money Where My Mouth Is!

Fidenza Macro - What will happen when the Reverse Repo Facility gets depleted?

ㅤ

👍 If you found this piece helpful, please give it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience.

Theme 3: The Week Ahead...

A quiet Friday morning session before the main event and as a result users of Harkster.com started their homework early, and were focused on The Week Ahead Channel and the previews filtering through....

Nomura Podcast - US, China and India CPI, FOMC and ECB Minutes, UK RICS and China Credit Data

S&P Global - Week Ahead Economic Preview: Week of 9 October 2023

ING - Asia week ahead: Regional inflation readings and an MAS decision

Theme 4: Look out for Friday Speedrun by Brent Donnelly

Brent has excelled himself once again, adding Friday Speedrun to his vast catalogue of publications (am/FX, Alpha Trader, 50 Trades in 50 Weeks and the Art of Currency Trading). Friday Speedrun is a concise read, an excellent review of the trading week, that is packed full of the key drivers and themes that dominated global markets. Brent's natural style and decades of experience on the sell and buy side makes this piece an easy read that is always thought provoking. The perfect recipe to add to @HarksterHQ's recommended reading list.

ㅤㅤ

ㅤㅤㅤ

Stay informed throughout the day with our new commentary feed (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

ㅤㅤㅤ

ㅤㅤㅤ

ㅤㅤㅤ

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

Rigged numbers ???

Supports the current Regime.....

6 Sigma.....Come On, Man !!!