Read on the Trading Floor - 02 Nov 2023

Today’s focus… US fixed income squeeze, US labour market ahead of NFP and much more…

Macro Themes At Play

Theme 1 - US fixed income rally has been driven by 5 elements....

The BoJ stepped in with an unscheduled bond auction ahead of 1%... this settled global duration.

A wave of soft / mixed US activity data followed weak global PMIs, with most European prints between 40-45.

The Atlanta Fed GDPNow forecast dropped to 1.2% for Q4, down from 2.3% on Oct 27

ISM Manufacturing hitting a disappointing 46.7 vs exp 49.

but has soft data been a resilient leading indicator... Brent Donnelly - Hard > Soft

The Treasury refunding announcement was not as "stark" as feared...

MacroVisor Breakfast Bites - "The Quarterly Refunding Announcement from the US Treasury showed that issuances at the long end are going to be less than expected. They said they will offer $112B in Treasury securities, up from $103B in the prior quarter, but a bit below some estimates for ~$114B."

FX Poetry Bulls Fondest Dreams - "The QRA indicated that the Treasury was going to issue a lot more T-Bills, a total of $1.1 trillion over the next two quarters, raising the proportion of T-Bills to 23.2%, even further above the old ceiling. Of course, the result is much less issuance in the 5yr and longer space, thus undercutting the excess supply argument...."

Investors were also encouraged by the Treasury QRA Statement anticipating “only one additional quarter of increases to coupon auction sizes”. This was a welcome change from their August statement that had referred to further coupon increases being likely needed “in future quarters”.

JPow delivered what was expected, missed some opportunities to be overtly hawkish on growth but left enough flexibility that hikes could still come if the data delivered. They did also add “tighter financial conditions” to the second paragraph.

Clarida on BBG TV "A problem with adding “financial” conditions to the statement is that they can go down as well as up.... Powell & Co. might regret including the word. And indeed, markets immediately loosened financial conditions by buying stocks and bonds."

Bloomberg - Bond Yields Fall: Don't Get Too Carried Away by the Treasury, Fed and BOJ - Bloomberg

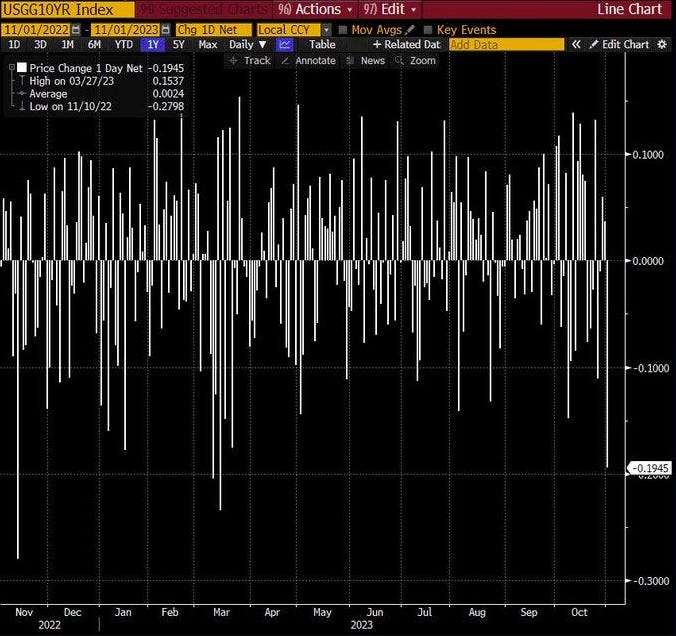

A position squeeze after the mid Oct pronouncements of 10s hitting 6% etc. The technical damage is extreme, US2s back below its 50sma, US10s falling away from 5%, 2s10s inverting (Stan vs Bill), whilst 10yr had their biggest daily drop since March.

SFRZ3Z4 - Higher for Longer theme correcting as more cuts get priced back into 2024

Source Bloomberg

When positioning gets turned: The large unwind of paid 10s trades has set in motion one of the biggest daily drops since March

Source Bloomberg via The BondBeat

Theme 2 - US labour market ahead of NFP

ECI 1.1% vs exp 1.0%

ADP adding jobs but fewer than expected ... 113k vs exp 150k.

ISM Manufacturing Employment Index ... 46.8 vs exp 50.3

Initial Claims a little softer at 217k vs exp 210k but until we see it at 300k over a 3-to-4-week spell, alarm bells aren't ringing yet.

Large pop in productivity lowers the unit labour cost -0.8% vs exp 0.7% (BMO)

Bloomberg's Whisper NFP: 203k vs survey of 180k

Given the reset to US growth expectations, the most important data point of the week will be tomorrow's NFP... will it add to the recession fears or rekindle Dec Fed pricing... ?

Initial claims are still showing no cracks, UER weaker over past few months due to increase in the Labour Participation Force

Source Bloomberg

Labour Force Participation continues to grow (retirees attracted back to the higher wages in the employment market)

Source Bloomberg

Theme 3 - Are financial conditions tightening?

The ex-Fed member Dudley via Bloomberg has questioned whether the Fed are doing the right thing by pausing - Federal Reserve’s Interest Rate Pause Could Go Terribly Wrong. In particular he draws the reader's attention to the following chart from A New Index to Measure U.S. Financial Conditions. FCI peaked in 2022, conditions aren't tight enough yet...

Steno Research also point to YoY easing in FCI - Something for your Espresso: How to deal with the new Fed feed-back loop?

👍 If you found this piece helpful, please give it a ‘Like’ at the bottom of the page. It only takes a few seconds and helps our free commentary reach a wider audience.

Top Pieces

Discovered on Harkster.com

Macro Hive - Equity View - Go Long Regional Banks and Homebuilders

Reuters - ECB reviews interest on government deposits to curb losses

Axios - Inside Israel's mission to attack Hamas, rescue hostages

Bloomberg - Israel, US Weigh Options for Gaza Strip’s Future, Including Peacekeepers

FT - Egypt-Hamas talks stalled on Gaza evacuation of foreign nationals

Apricitas Economics - America's Return to Strong Growth drivin by rising household consumption, significant inventory buildups and a steady recovery in government output.

Brent Donnelly am/FX - Big Diff... USD underreacting to the move in yields, so far

ING FX Daily - Fed pause renews interest in the carry trade

ABN Amro - Ripple effects: Exploring the impact of low Rhine water levels on the Dutch economy

ING - Bank of England keeps policy steady but pushes back against rate cut expectations

ㅤㅤㅤ

Stay informed throughout the day with our new commentary feed (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

ㅤㅤㅤ

ㅤㅤㅤ

ㅤㅤㅤ

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

thanks for the shout out. in truth, the biggest surprise to me is that gold is lagging here