Read on the Trading Floor - 02 April 2024

Today’s focus… China, US > EU, Tesla, Q2 stock outlook and much more

Macro Themes At Play

Theme 1 - Softer inflation in Europe plays into the ECB's hands

Theme 2 - Can we believe the strength in Manufacturing PMI's?

Theme 3 - Can the rally continue in Q2?

Theme 4 - Going long China?

Further reading and listening of note

Theme 1 - Softer inflation in Europe plays into the ECB's hands

ECB's survey of median expectations for inflation over the next 12 months decreased to 3.1% from 3.3%. Now at its lowest level since Feb '22 and the start of Russia’s invasion of Ukraine. The 3yr ahead remained unchanged at 2.5%. (ECB Consumer Expectations Survey results – February 2024). Along with German inflation printing lower and in line with expectations (down to 2.2% from prior 2.5%), following on from the gap down in French data, the Q2 cut from the ECB after the SNB already cut has energised the RV rates trade (REC EU2s vs PAID US2s). However, it's been a fixed income play rather than an FX trade. Even today, after opening at the lows, EURUSD has drifted back towards 1.0800, barely down 2/3% on the Jan 1st opening levels.

ECB members have guided us to a Q2 cut and the data has backed it up. In the US it's hard to argue the same regime has occurred. The resilient US data has the Fed back pedalling a little (Waller/Powell) whilst Bostic has already indicated that 1 cut maybe enough. As a result, ING highlight that the rate spread (around 145bps) is now at the most supportive for the USD since Dec 2022. We hear from a plethora of members this week, starting with Williams (17:00), Mester (17:05) and Daly (18:30) but it will be the data (ISM, nfp and CPI) that will allow Powell to cut before the Presidential elections or not.

Bloomberg - Rate Cuts: Points of Return’s Year of Descending Dangerously — Divergence

Macro Musings - Isabel Schnabel on the ECB and its New Operational Framework

Theme 2 - Can we believe the strength in Manufacturing PMI's?

Q2 has started with a wave of stronger than expected manufacturing PMI prints. For example, March marked the first monthly expansion for US manufacturing since September 2022 with the PMI rising > 50.

Chinese Caixin: 51.1 vs prior 50.9 and exp 51

US ISM Manufacturing: 50.3 vs prior 47.8 and exp 48.4

India PMI: 59.1 vs prior 56.9 and exp 59.4

Spanish: 51.4 vs prior 51.5 and exp 51

French: 46.2 vs prior 47.1 and exp 45.8

German: 41.9 vs prior 42.5 and exp 41.6

UK: 50.3 vs prior 47.5 and exp 49.9

The question is whether one should believe the soft data, will this time be different? The surveys have clearly been distorted by the covid reopening / fiscal impulse / near-shoring regime that we've passed through, but with FCI so soft, why would manufacturing not be improving? In addition, we're another quarter away from the re-opening so the surveys should also be normalising.

FX Poetry by Andy Fately - Dismay

Brent Donnelly am/FX - Taking a shot at short USD

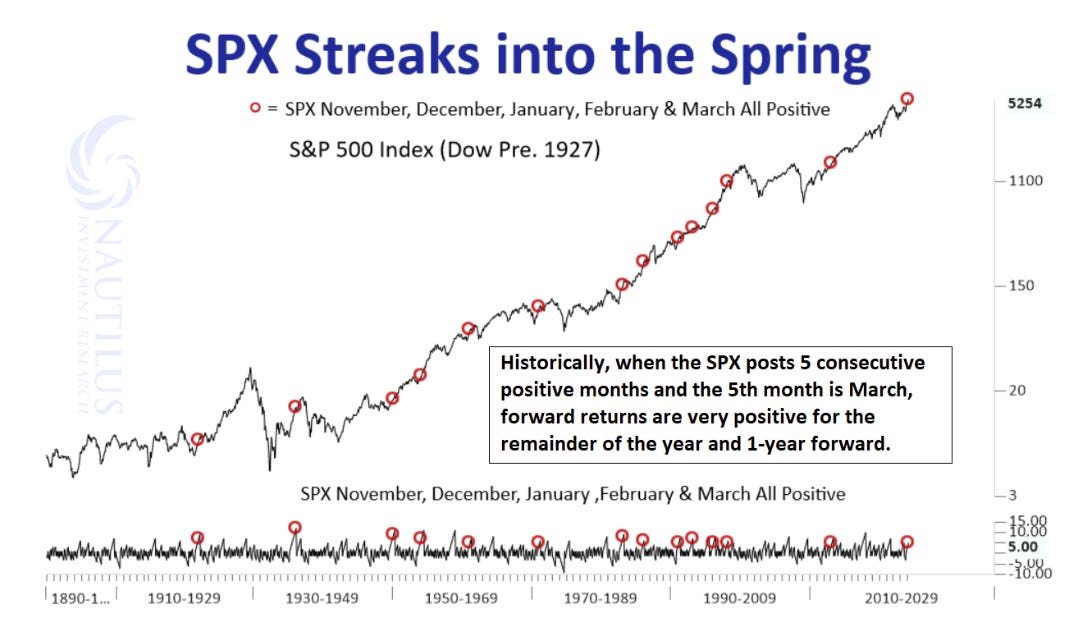

Theme 3 - Can the rally continue in Q2?

The data says it can. Nautilus Research (SPX 'Streaks' Into the Spring) highlight the following facts....

After a warm financial winter, the average 1-year forward return has been a robust 15.01% up, which notably outpaces the general average of 7% up seen over all periods.

13 out of 14 events following this trend resulting in an upswing for the remainder of the year.

In essence, the pattern is clear and historically grounded: when the SPX joyfully leaps into spring with five consecutive months of gains, the market tends to ride this wave of optimism, resulting in notable growth for investors by year's end and even into the next year.

Theme 4 - Going long China?

On a day when Tesla miss, Xiaomi it's cheaper alternative has hit the headlines as it's $30k car looks a gamechanger in the EV sector and will further compress pricing in the sector. Xi's QE comments are also garnering a lot of attention, the market after all loves a QE story let alone the big fiscal impulse that everyone has been hoping for from the East. The headwinds for Chinese assets are steadily reducing and some funds have started to rotate or rebalance away from the long India / Short China trade.

The MacroTourist by Kevin Muir - HUKOU REFORM: THE NEXT CHINESE STIMULUS?

Bloomberg - Xiaomi SU7 EV Is Proving a Winner With Investors in Hong Kong

Bloomberg - Xi’s Speech Suggests PBOC May Start Trading Government Bonds

SCMP - Xi Jinping to China’s central bank: restart treasury-bond trade, after 2-decade hiatus

SCMP - China’s central bank keeps ‘cautious’ in bond trade despite Xi Jinping’s mandate

Bloomberg - Investors Who Bought India, Sold China Are Starting to Unwind the Trade Strategy

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

Top Pieces

Discovered on Harkster.com

FT - Tesla shares sink after sales fall more than expected in first quarter

Russell Clark - MARCH NEWSLETTER AND REVIEW - A good month for inflationary assets.

CreditNews - It’s now cheaper to rent than to buy a home in America’s top cities

Morningstar - DJT Stock: Trump Media Isn’t a Meme Stock, It’s a Cryptocurrency

FT - In charts: the quarter when central banks wrong-footed the markets

Unchained - Is the SEC Preparing for a Fight Against Ethereum?

Man Group - Views from the Floor - Going Against the Grain

Bloomberg - Crash or Soar? Traders Are Preparing for Stock Market Extremes

Compound Quality - 10 Quality Stocks

Stay informed throughout the day with our new commentary channel (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

thanks for the shout out!