Morning Call Script - 31 Oct 2023

Overnight asset drivers & the impending data calendar

What’s Moved Overnight

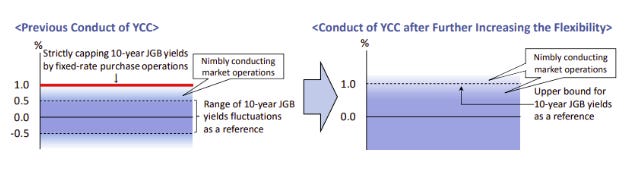

1%... The BoJ's new "reference" point after they raised their inflation forecasts across the board 2023 to 2.8% (prior 2.5%), 2024 to 2.8% (prior 1.9%) and 2025 to 1.7% (prior 1.6%).

“It is appropriate for the Bank to increase the flexibility in the conduct of yield-curve control, so that long-term interest rates will be formed smoothly in financial markets in response to future developments."

They will "nimbly" work either side of 1%... The BoJ have redefined their limit as an "upper bound" rather than a rigid target

Bloomberg - YCC Verdict: Bank of Japan Is Guilty of a Messaging Mistrial

Nikkei - BOJ drops explicit 1% ceiling for 10-year JGB yields

USDJPY back above 150.00 as US fixed income now seen as the key driver ahead of Fed and Treasury issuance

Ahead of Wed refunding plan, the UST said they expect to borrow $76bln less than July

Reuters - US Treasury cuts Oct-Dec borrowing estimate to $776 bln, yields ease

China's PMIs missed expectations in October, manufacturing slipping back into contraction territory (49.5 vs Sept 50.2). AUD, CNH, HSI, CSI ... all in decline following the disappointing data set

Have a great day, and keep smiling!

Podcast for the Commute

The Day Ahead

EUR (10:00): GDP

EUR (10:00): Inflation Rate

CAD (12:30): GDP

USD (12:30): ECI

Stay informed throughout the day with our new commentary feed (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

ㅤㅤㅤ

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.