Harkster Preview - BoJ Dec 18th

Today’s focus... should I set my alarm?

Consensus

A meeting too soon. Negative rates to remain in-situ, YCC to also remain via the 1% (errr 97bps) implied cap. The surprises would come if they were to prematurely hike, or if they left rates unchanged but pre-signaled a January hike.

Hawk = Early rate hike out of negative territory

Semi Hawk = unchanged but pre-signal Jan or April hike

Dove = unchanged, no fwd guidance, wait for wage agreements

With one eye on Xmas festivities and the pnl mark effectively set for 2023, there's as a sense of dread in London

Option 1 - If I don't set my alarm to keep an eye on Nikkei releases (3 of the 5 meetings under Ueda have had pre-announced sourced stories in the Nikkei hours before the official meeting release) then the BoJ will shock the mkt and lift rates out of negative territory.

Option 2 - If I do set my alarm, it will be a snoooooozzzzer and all we get is a pop back to USDJPY 144.00ish, nothing to materially move the needle and change the year end performance.

Why is it a meeting too soon...?

The BOJ added flexibility to its YCC at the meeting in October... rare to see back-to-back changes

The BoJ will not have new staff forecasts at this meeting

The Shinto wage agreements have not been reached.

They normally take place in the spring, and like the ECB / BoE, are a key component for a decision to change track. (FT - Hawkish ECB rate-setter says wage ‘slowdown’ key to timing of policy shift).

For CB's (well for those that have yet to pivot like the Fed), all it will take is a bull market in oil (are we at range lows sub $70?) as well as decent wage gains in Q1 2024 to get headline inflation higher.

There is no expectancy trade in the 10yr JGB (chart below) ... drifting sub 70bps.

Hard to see a pivot before an election year, given the momentous interest rate payments to be made if bonds do pop into positive territory...

Domestic politics are already heading towards an early election, could Kishida step down by spring? He already has a record low approval rating.

The Fed exit disrupts the JPY feedback loop #ccywars - could they hike in April when the Fed cuts for the first time?

The next BoJ meeting is not too far away. The 23rd of Jan meeting will offer them the chance to see two CPI reports and their new staff forecasts.

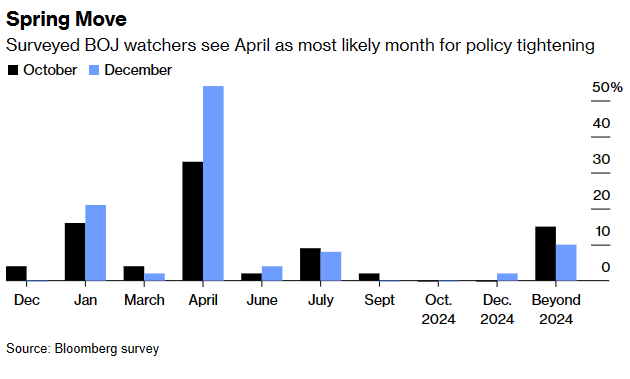

Market consensus aligns with former BoJ Nagai's comments = "The most likely timing of an exit is in April, after which the BOJ will probably guide short-term rates in a range of zero to 0.1%".

2/3rds of economists expect the BoJ to hike by April (Bloomberg Survey)

As the consensus surveys show (Reuters), the focus should be on the Japanese year end for BoJ policy change. Although that timing post wage agreement is natural in a vacuum, it is distorted by the political situation in Japan (early election risk) as well as the market pricing Fed cuts by March.

How have the BoJ guided us towards tomorrow's meeting, what have they said?

#1. After adjusting to an implicit level around 1%, the 10yr JGB got within 3bps of the threshold only for the BOJ to step in and announce an unscheduled buying operation. Many in London expected them to allow 1.00% to break, clear out the stops and then come in forcefully, but they got ahead of the level and showed they still weren't comfortable with the "uncapped" YCC.

#2. Ueda's comments on Dec 07 (BIS)

Ueda got the market excited (BBG - Trader's piled into bets), or did we simply find the soft side (Weston Nakamura - Potential JPY surge) as the stars aligned... short gamma exposure, US10s rally, cta stops, forced unwind of carry trade, Dec USD seasonals etc etc ...

#3. BOJ IS SAID TO SEE LITTLE NEED TO END NEGATIVE RATE IN DECEMBER

It didn't last long, although long enough to clean out the market but it was walked back by source stories relatively swiftly.

ZeroHedge - Yen Plummets On Report BOJ Will Not Hike Rates Any Time Soon

Bloomberg - BOJ Is Said to See Little Need to End Minus Rate Next Week

For all the BoJ / Fed chatter .... USDJPY = US yield story.

10yr sub-4%... that's what's driven the last leg and how much more can we ask for the 10year? Will it stick sub 4%? We're entering a period, when seasonals point to higher yields. The last few weeks of a year, ahead of a wave of Q1 issuance can put pressure on rates markets as portfolios make room for new paper. Furthermore, if the Fed has gone too early when those with softer growth dynamics are pushing back, could we see a steeper curve to fit reignited inflation? Finally, January will also bring Yellen's next funding announcement for the treasury.

Bloomberg - BMO Sees 10-Year Treasuries Retesting 5% With Volatile 2024 on Tap

Steno Research - Bull Steepening Watch - Is lower yields really what risk assets?

Capital Flows and Asset Markets by

- HAS INFLATION BEEN CONQUERED?- - Friday Speedrun... "If you believe the Fed Pivot is inflationary, you should be selling bonds aggressively here"

Furthermore, there is a potential rhs M&A (FT - Nippon Steel agrees to buy US Steel for $14.9bn) as well as 10s being overbought sub 4% and we could have a 1-2% "dovish BoJ" trade for those left behind on the desk to play with.

Source: MarketWatch

Where can the surprise come from? Let's be honest, Ueda has had a penchant to surprise

Across The Spread by

- December Bank of Japan Preview: YCC Is (Already) DeadBank of Japan will “declare” (or, purposely un-muddle and explicitly clarify) that Yield Curve Control by NAME is no more. And if I am correct in both the policy communication assessment, AND the markets coming to realization (or BOJ bringing markets to realization) of an already dead YCC policy - we may get fireworks in markets, namely a major sell off in JGBs / surge in yields, and another) vicious short squeeze in JPY - the degree to which will be dependent on just what proportion of market participants out there are unaware that YCC is already dead.

Why wait for the wage agreements...

What's in the price?

Markets see a 40% probability of a 10bps hike in January

10yr JGBs drifting into the meeting sub 70bps... no pressure or indication that anything is expected domestically tomorrow.

Source: MarketWatch

👏 If you found this briefing helpful, please show the desk some appreciation by giving it a ‘Like’ or a ‘Comment’ at the bottom of the page.

Top Sources

Discovered on Harkster.com

BoJ Previews that have arrived in our curated BoJ channel on Harkster.com:

Steno Research - 5 (+1) CENTRAL BANKS WE WATCH – FED, ECB, BOE, NORGE’S BANK, BOJ & BCB

am/FX by Brent Donnelly - BOJ and Yields

Saxo Bank - Macro and FX: Watch USD sentiment and BoJ hints on rate policy

Reuters - Japan's central bank to sit tight on policy, may drop hints on pivot

Bloomberg - BOJ Isn’t Ready for a Requiem to the Negative-Rate Era

The Lead-Lag Report - What Could Tightening By The Bank of Japan Look Like?

Nomura - The Week Ahead – BOJ Meeting, UK CPI and US PCE Deflator

ING - Japanese data improves but we still don’t expect a BoJ policy shift this month

Stay informed throughout the day with our new commentary feed (‘Intraday Market Colour’) highlighting key notes, topics du jour, and HarksterHQ’s market updates around key data points and headlines.

Available on the Harkster Research Platform.

The information provided in this post is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

Excellent summary!